IDTechEx find industrial and commercial EVs are the winners

2013年11月15天

IDTechEx find industrial and commercial electric vehicles are the winners

By Dr Peter Harrop, Chairman, IDTechEx

As the electric vehicle EV industry grows more than five-fold to well over $300 billion in 2024, those e-vehicles not bought primarily on up-front price will continue to dominate. These are the large vehicles such as buses and military vehicles and the heavy lifting or pushing vehicles such as forklifts and earthmovers. The customers here are companies and government primarily concerned about Total Cost of Ownership (TCO) and performance. Less important are private individuals with their great concern about up-front price when they buy their smaller or lighter duty vehicles such as e-cars, e-boats and e-bikes.

Industrial and commercial is the largest sector

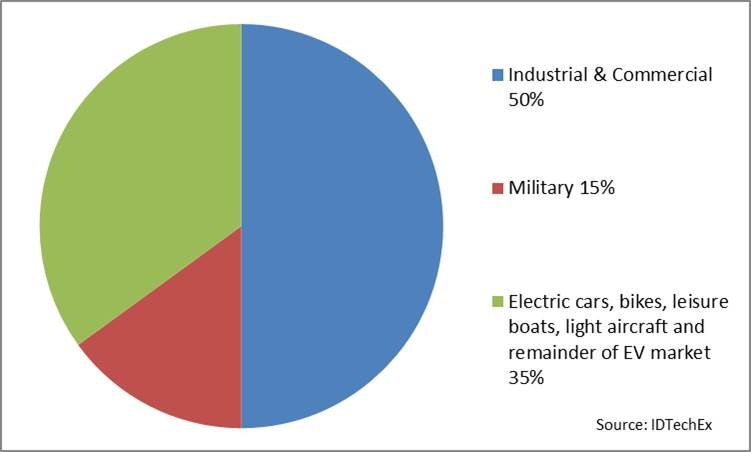

IDTechEx  forecast that over the next decade, the largest global EV value sector will be industrial and commercial for land, water and air - accounting for nearly 50% of the total hybrid and pure electric vehicle business. It is fully analysed in the IDTechEx report, Industrial and Commercial Hybrid & Pure Electric Vehicles 2013-2023: Forecasts, Opportunities, Players.

forecast that over the next decade, the largest global EV value sector will be industrial and commercial for land, water and air - accounting for nearly 50% of the total hybrid and pure electric vehicle business. It is fully analysed in the IDTechEx report, Industrial and Commercial Hybrid & Pure Electric Vehicles 2013-2023: Forecasts, Opportunities, Players.

Personal electric cars, bikes, leisure boats, light aircraft and so on will be about 35% of the EV business to 2024. Military e-vehicles, land, water and airborne will be most of the remaining value market in 2024 and, as with industrial and commercial ones, they are not bought primarily on up-front price.

The total hybrid and pure electric vehicle market in 2024 (figures rounded)

Easier to make money

Manufacturers of industrial and commercial electric vehicles and their parts and services tend to be profitable whereas those making personal electric bikes and cars report the most losses and bankruptcies. That said there are far too many manufacturers of light industrial and commercial e-vehicles. Their profitability can be improved even further by mergers and a shakeout of those that are neither niche nor volume players, as happened in the heavy lifting pulling or pushing industrial and commercial sector with electric forklifts, ten years ago. These disparate vehicles could also share a common platform in many cases, saving cost and increasing reliability.

Main market will be industrial and commercial on land

The electric vehicle business is primarily an industrial and commercial business and, within that category, land-based applications will continue to predominate, split fairly evenly between "on" and "off-road" versions, that remaining the case throughout the coming decade as both subsectors add substantial new applications.

Marine industrial and commercial is substantial

Within the overall industrial and commercial category, marine industrial and commercial vehicles come second to land based ones. Marine industrial and commercial includes pure electric Autonomous Underwater Vehicles AUV, hybrid tugboats and pure electric and hybrid ferries on both the sea and inland water ways. Closely allied are the electric thrusters that move the largest ships sideways when berthing and ones that let tugboats hold position purely electrically while waiting to tow at sea.

Buses will remain the biggest on-road industrial and commercial value market

Within the on-road types, buses are particularly important industrial and commercial vehicles primarily due to the massive program of the Chinese government. Next come e-vans/delivery trucks, conventional electric cars and special designs used as taxis and converted golf cars used as people movers in airports, theme parks and hotel grounds.

Indoor forklifts remain the biggest off-road industrial and commercial value market

Off-road, IDTechEx assess in the report that indoor forklifts will continue to be the main subsector of industrial and commercial vehicles but with largest growth from relatively new applications such as agriculture, mining, utility and construction vehicles and outdoor forklifts, all of which are usually hybrids in order to cope with tough duty cycles.

Numbers and dependency

The industrial and commercial EV sectors each involve well under one million vehicles yearly, in contrast to the over one million e-cars or mobile robots sold yearly, and the tens of millions of yearly sales seen with e-bikes. With industrial and commercial electric vehicles, as with military ones, purchasing decisions by governments and companies are key, whereas with personal e-vehicles, and particularly with pure electric cars, the far less trustworthy subsidies and tax breaks by governments are essential for at least eight more years if they are to become viable, substantial businesses.

Watch the migration

Not surprisingly then, the more savvy players start or move across to the more prosperous, larger gross value industrial and commercial sector - examples include SAFT, Altairnano and EnerSys making industrial and commercial vehicle traction batteries and Siemens making electric motors, motor controls and inverters and those making energy harvesting like Levant. Rogers Corporation directs its Directly Bonded Copper (on ceramic) DBC to the industrial and commercial EV sector. Maxwell Technologies mainly sells its traction supercapacitor banks into electric buses in China and WIMA sells similar banks for energy harvesting into hybrid construction vehicles. Nissan has recently bought a large electric forklift company lifting it to number six in what is currently the largest industrial and commercial EV subsector and where the top twenty usually make good profits.

Hotbed of innovation

Thanks to the Nidec subsidiary SR Motors, the first major trials of switched reluctance traction motors have been in agricultural and construction e-vehicles. Only much later will the Bosch/Prodrive research lead to their use in private cars. The most impressive adoption of in-wheel electric motors has been in buses and trucks and considered essential for Extremely Short Take-off and Landing ESTL small commercial aircraft such as air taxis expected near the end of the coming decade. The new SiC and GaN power components will first appear in large industrial and commercial vehicles, as will energy harvesting shock absorbers driving electrically active suspension and charging traction batteries. To some extent this is because such devices are most suited to these vehicles but it is also because the industrial and commercial electric vehicle sector is the most secure, with money to spend and paybacks without the need of subsidy. Where, as here, up-front cost is not critical, more innovation takes place and advanced components are adopted profitably for all concerned.

Market drivers

The market drivers for hybrid and pure electric industrial and commercial vehicles can, in the main, be divided into reduced Total Cost of Ownership TCO, better performance and government action that bans or severely restricts noisy and/or polluting vehicles from certain locations, such as harbours, and forbids any piston engined boats on an increasing number of inland lakes from Taiwan to Germany. Those performance improvements include tugboats, construction and utility vehicles delivering instant maximum power, some acting as electrical power sources at destination and reliability and long life. Add to that the need to respond to changes in society such as more ordering on-line leading to more home delivery by truck and an increasing number of people managing without a car and an increasing percentage of the elderly in cities remaining mobile, both of which lead to more buses and taxis being required. For example, the German Government and its car industry agree that there will be fewer cars in Germany in ten years from now.

Payback is often relatively unimportant

New and tighter laws, modest subsidies, tax breaks boosts the industrial and commercial EV market. This is true even where payback is long at say eight years or even non-existent. In addition, by buying these electric vehicles, local and national government seeks a green image and wish to reduce local noise and air pollution. Most countries ban internal combustion engines from enclosed spaces and the USA even bans their use in some orchards. Consequently, almost all indoor forklifts in the world are electric, the highest percentage being in Europe and the lowest percentage being in East Asia. On road, an increasing number of countries introduce onerous pollution requirements for vehicles to reduce pollution wherever they are, usually with the secondary benefit of reducing dependence on foreign oil.

In contrast to electric cars, encouraging a green agenda costs relatively little with industrial and commercial vehicles. In 2012, the U.S Department of Energy invested a modest $10 million in the development of battery-electric trucks, forklifts and other cargo vehicles to cut petroleum use by the domestic transportation industry. 50% of the development of particular technologies that related to cargo vehicle electrification was offered. New standards require semi-trucks to cut fuel use and emissions by 20% by 2018, while heavy-duty vans and pickups must cut fuel use by 15%. Buses and garbage trucks must reduce fuel use by 10%. This cuts $50 billion in fuel expenditures and saves 530 million barrels of oil.

Read the full IDTechEx report, Industrial and Commercial Hybrid & Pure Electric Vehicles 2013-2023: Forecasts, Opportunities, Players.