Despite Concerns Rare Earth Free Motors Take a Back Seat in EVs

Mai 23, 2024

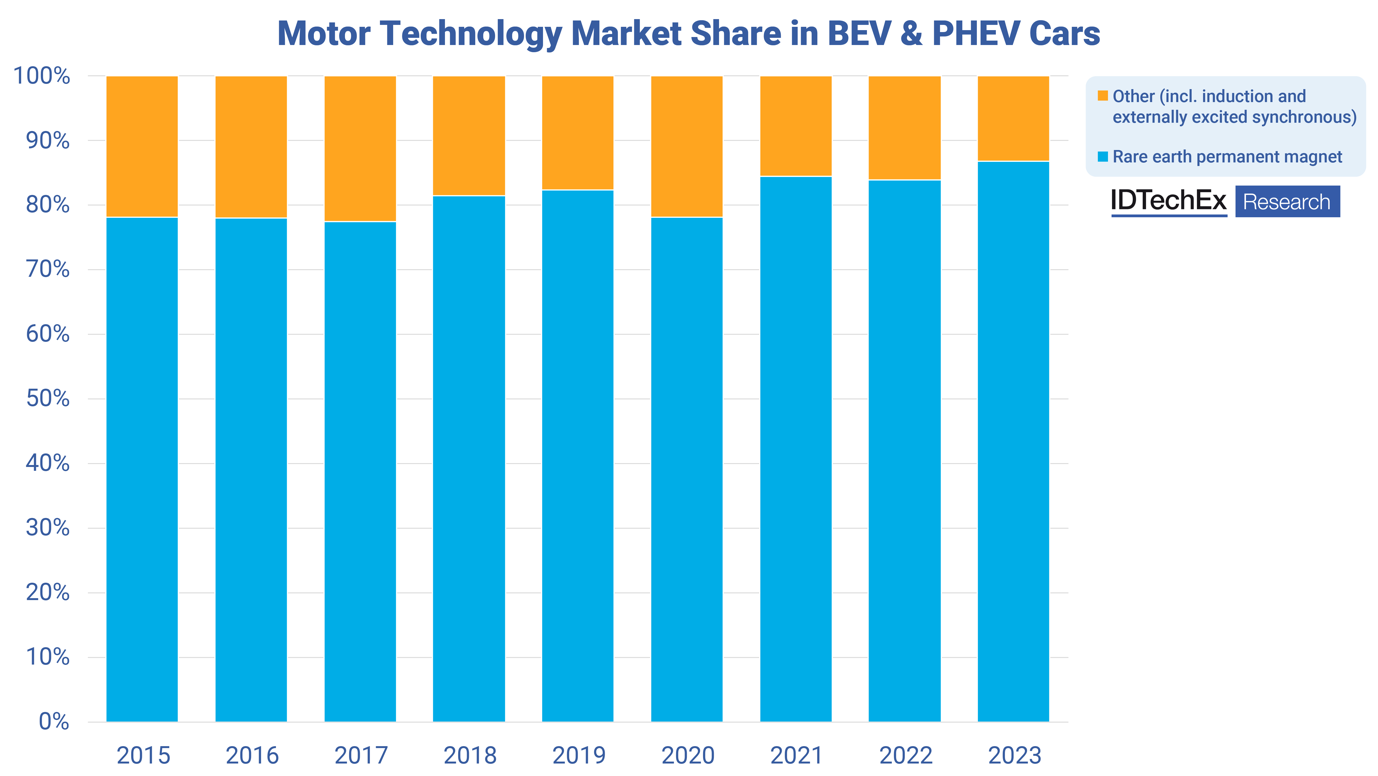

The sourcing of materials and components is becoming an increasingly discussed topic across multiple industries. One huge growth sector is the electric vehicle (EV) market, with IDTechEx predicting 4 fold growth in electric car sales over the next 10 years. Much of the conversation is focused on battery materials, but the rare earths used in the magnets in electric motors are another key concern. These are almost entirely produced in China and have been subject to significant historic price volatility. Given these concerns, it is surprising to see that IDTechEx's research has found that rare earth permanent magnet motors have maintained over 77% of the electric car market over the last 9 years. Why is that the case?

Motor technology market share in BEV and PHEV Cars. Source: IDTechEx

The IDTechEx report "Electric Motors for Electric Vehicles 2024-2034" predicts that over 140 million electric motors will be required for EV markets. While it predicts a decline in the market share of rare earth motors, it predicts that the majority of the market in 2034 will still be using permanent magnet motors.

What are the concerns?

China largely controls the supply of rare earth materials, and this has historically led to significant price volatility. In 2011, after China restricted its exports of rare earths, the price of neodymium and dysprosium rose by approximately 750% and 2000%, respectively. Prices rose again in 2021 and 2022 to a peak in 2022 of around 4 times its average over the previous 8 years. While the price settled again in 2023 and the start of 2024, this remains a concern for the future.

Local sourcing of materials and improving domestic supply chains have become an increasing focus for many industries and governments that want to secure their future. As an example, the US has allocated resources to improving its domestic supply of rare earths, but it will take time to bring these ventures online.

Rare earths also present environmental concerns around mining and processing, and the waste generated in doing so.

What is the state of the market and technology?

Permanent magnet motors remain the dominant technology in EVs. Thanks to the previously mentioned concerns, there has been progress with rare earth free alternatives. Renault has used externally excited synchronous motors (EESM) in EVs since the Zoe, and other manufacturers like BMW have adopted this approach. However, while these motors reduce the material costs, their manufacturing is typically more complex thanks to copper windings on the rotor and the need for rotor excitement. Hence, manufacturing costs are typically higher.

Rare earth free magnets are another solution, at varying levels of commercial readiness, with companies like Proterial stating its magnets "deliver the world's highest levels among ferrite magnets". Niron Magnetics is developing iron nitride magnets, with its next-generation versions planning to rival neodymium performance. PASSENGER is a European project developing strontium ferrite and manganese aluminum carbon alloys. There are significant efforts in this arena, and while these materials are unlikely to be a like-for-like replacement for rare-earth magnets in the near future, the benefits of lower cost and supply stability could be enough to swing the market in this direction, with IDTechEx predicting a 12% share for rare earth free magnets in the market by 2034.

Why permanent magnet motors remain the dominant technology

There are two primary factors (with multiple considerations therein) that drive the choice of motor technology: performance and cost. Rare earth permanent magnet motors tend to provide the highest power and torque density, efficiency, and low manufacturing costs. Their major downfall is the bill of materials costs, with the magnets often accounting for around a third of the total motor material costs.

From their 2022 peak, rare earth prices have settled, leading to permanent magnet motors becoming cost-competitive again and taking some of the immediate emphasis away from the need for alternatives. Most tier 1 suppliers now offer the option for permanent magnet motors or EESMs, but it is down to the OEM to make that commitment. From IDTechEx's interviews with OEMs, most have available options for EESMs in-house or through suppliers, but they are mostly reserved in case magnet prices rise significantly or the need to localize material supply increases (through geopolitical or regulatory pressure).

A larger question

Unless we see a significant improvement in rare earth free magnets, or a large regulatory push, rare earth permanent magnet motors are likely to retain the majority of market share, especially given China is the largest EV market and has less incentive to move away from rare earths.

One question that should be asked is whether drivers really need as much power as is often installed in vehicles or dual motor variants? Dual motor variants are typically less efficient and utilize more materials to create and install the second motor. These higher powers and extra motors are not needed for the vast majority of the time, much like larger vehicles in general. However, the more powerful, higher trim models appeal to a different consumer demographic and give OEMs an opportunity to increase their profit margins. If this helps EVs gain further market share, displacing combustion engines, then perhaps this is the lesser of two evils.

IDTechEx's report, "Electric Motors for Electric Vehicles 2024-2034", takes a deep dive into the types of electric motors used in electric vehicles as well as emerging alternatives like axial flux and in-wheel motors. The report considers the EV market for cars, buses, trucks, vans, two-wheelers, three-wheelers, and microcars across China, Europe, and the US, including forecasts for motor demand by technology and materials used over the next 10 years.

To find out more about this IDTechEx report, including downloadable sample pages, please visit www.IDTechEx.com/motors.

For the full portfolio of electric vehicle market research from IDTechEx, please see www.IDTechEx.com/Research/EV.

IDTechEx provides trusted independent research on emerging technologies and their markets. Since 1999, we have been helping our clients to understand new technologies, their supply chains, market requirements, opportunities and forecasts. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.