This report has been updated. Click here to view latest edition.

If you have previously purchased the archived report below then please use the download links on the right to download the files.

Graphene, 2D Materials and Carbon Nanotubes: Markets, Technologies and Opportunities 2016-2026

Granular ten-year market forecasts, data-driven and quantitative application assessment, 60+ interview-based company profiles, revenue/investment/capacity by player, and more

| 1. | INTRODUCTION |

| 1.1. | There are many graphene types |

| 1.2. | Many ways of producing graphene |

| 1.3. | Explaining the main graphene manufacturing routes |

| 1.4. | Morphologies of graphene on offer |

| 1.5. | Market conditions, trends and outlook |

| 1.6. | General observations on the market situation |

| 1.7. | Moving past the peak of hype |

| 1.8. | Supplier numbers on the rise |

| 1.9. | Media attention and patent publications on the rise |

| 1.10. | Large scale investment in graphene research |

| 1.11. | Investment in graphene company formation |

| 1.12. | Revenue of graphene companies |

| 1.13. | The industry is still in the red |

| 1.14. | Initial public offerings |

| 1.15. | Information on supplier morphology, investment & revenue |

| 1.16. | The rise of China |

| 1.17. | China was successful in carbon nanotubes |

| 1.18. | Patent trends |

| 1.19. | Graphite mines see opportunity in graphene |

| 1.20. | Production capacity by player |

| 1.21. | The importance of intermediaries |

| 1.22. | Graphene Prices and Pricing Strategy |

| 1.23. | Quality and consistency issue |

| 1.24. | Graphene application pipeline |

| 1.25. | Graphene-enabled products and important prototypes |

| 1.26. | Benchmarking graphene suppliers |

| 2. | MARKET PROJECTIONS |

| 2.1. | Granular ten year graphene market forecast |

| 2.2. | Ten year graphene market forecast |

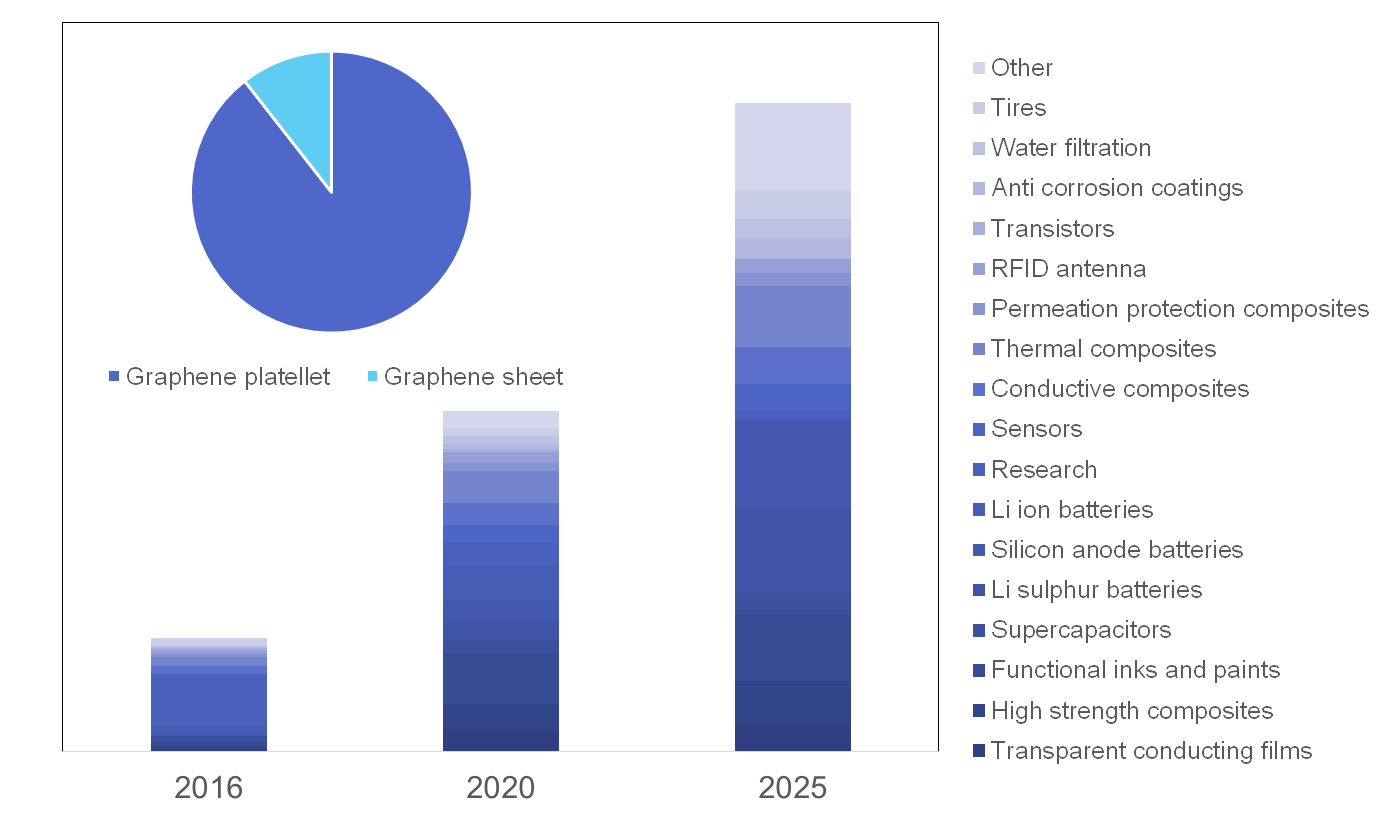

| 2.3. | Forecast for graphene platelet vs sheets |

| 2.4. | Graphene market in 2019 |

| 2.5. | Graphene market in 2026 |

| 2.6. | Forecast for volume (MT) demand for graphene platelets |

| 3. | GRAPHENE PRODUCTION |

| 3.1. | Expanded graphite |

| 3.2. | Reduced graphene oxide |

| 3.3. | Oxidising graphite |

| 3.4. | Reducing graphene oxide |

| 3.5. | Direct liquid phase exfoliation |

| 3.6. | Direct liquid phase exfoliation under shear force |

| 3.7. | Electrochemical exfoliation |

| 3.8. | Properties of electrochemical exfoliated graphene |

| 3.9. | Plasma exfoliation |

| 3.10. | Substrate-less CVD |

| 3.11. | Substrate-less CVD (plasma) |

| 3.12. | Chemical vapour deposition (CVD) |

| 3.13. | Chemical vapour deposition |

| 3.14. | Transfer process for chemical vapour deposition |

| 3.15. | Roll-to-roll transfer of CVD graphene |

| 3.16. | Novel methods for transferring CVD graphene |

| 3.17. | Sony's approach to transfer of CVD process |

| 3.18. | Sony's CVD graphene approach |

| 3.19. | Wuxi Graphene Film Co's CVD graphene progress |

| 3.20. | Direct growth of CVD on SiOx? |

| 3.21. | Production cost of CVD graphene |

| 3.22. | Epitaxial |

| 3.23. | Largest single-crystalline graphene reported ever |

| 4. | GRAPHENE MATERIALS |

| 4.1. | Pictures of graphene materials |

| 5. | GRAPHENE APPLICATIONS AND MARKETS |

| 6. | TRANSPARENT CONDUCTIVE FILMS |

| 6.1. | Indium Tin Oxide |

| 6.2. | Market forecast for transparent conducting films |

| 6.3. | Performance of ITO films on the market |

| 6.4. | Production cost and flexibility of ITO films |

| 6.5. | Supply and demand for ITO films and indium |

| 6.6. | Changing TCF market dynamics and needs |

| 6.7. | Assessment of ITO alternatives |

| 6.8. | Graphene performance as TCF |

| 6.9. | SWOT analysis on graphene TCFs |

| 6.10. | Performance of silver nanowire TCFs |

| 6.11. | Flexibility of silver nanowire TCFs |

| 6.12. | Silver nanowire TCF cost structure |

| 6.13. | Silver nanowire products on the market |

| 6.14. | Metal mesh TCF performance |

| 6.15. | Flexibility of metal mesh TCFs |

| 6.16. | Performance of carbon nanotube TCFs |

| 6.17. | Useful information on carbon nanotube TCFs |

| 6.18. | Benchmarking TCF technologies |

| 6.19. | Make or break year for ITO alternatives? |

| 6.20. | Consolidation period for the ITO alternative market |

| 6.21. | ITO alternative ten-year market forecast |

| 7. | GRAPHENE CONDUCTIVE INKS |

| 7.1. | Performance of Graphene conductive inks |

| 7.2. | Applications of conductive graphene inks |

| 7.3. | Resistive heating using graphene inks |

| 7.4. | De-frosting using graphene inks |

| 7.5. | De-icing using graphene heaters |

| 7.6. | Transparent EMI shielding |

| 7.7. | Graphene-enabled products and important prototypes |

| 7.8. | Graphene inks can be highly opaque |

| 7.9. | RFID types |

| 7.10. | RFID antenna market figures |

| 7.11. | RFID antennas |

| 7.12. | Cost breakdown of RFID tags |

| 7.13. | Methods of producing RFID antennas |

| 8. | SUPERCAPACITORS |

| 8.1. | Ten-year market forecast for supercapacitors by application |

| 8.2. | Application pipeline for supercapacitors |

| 8.3. | Cost structure of a supercapacitor |

| 8.4. | Cost breakdown of supercapacitors |

| 8.5. | Supercapacitor electrode mass in transport applications |

| 8.6. | Addressable market forecast for supercapacitor electrodes |

| 8.7. | Supercapacitor performance using nanocarbons |

| 8.8. | Performance of existing commercial supercapacitors |

| 8.9. | Challenges with graphene |

| 8.10. | Graphene surface area is far from the ideal case |

| 8.11. | Promising results on graphene supercapacitors |

| 8.12. | Performance of carbon nanotube supercapacitors |

| 8.13. | Potential benefits of carbon nanotubes |

| 8.14. | Challenges with the use of carbon nanotubes |

| 8.15. | Electrode chemistries of supercapacitor suppliers |

| 9. | ENERGY STORAGE |

| 9.1. | Historical progress in Li ion batteries |

| 9.2. | Quantitative benchmarking of Li and post-Li ion batteries |

| 9.3. | Quantitative benchmarking of Li and post-Li ion batteries |

| 9.4. | EV numbers used in this projections |

| 9.5. | Electrode mass by battery type |

| 9.6. | Cost breakdown of Li ion batteries |

| 9.7. | LFP cathode improvement |

| 9.8. | Why graphene and carbon black are used together |

| 9.9. | Graphene improves NCM battery cathode |

| 9.10. | LiTiOx anode Improvement |

| 9.11. | How CNT improve the performance of commercial Li ion batteries |

| 9.12. | Why graphene helps in Si anode batteries |

| 9.13. | State of the art in silicon-graphene anode batteries |

| 9.14. | Samsung's result on Si-graphene batteries |

| 9.15. | State of the art in silicon-graphene anode batteries |

| 9.16. | Why graphene helps in Li sulphur batteries |

| 9.17. | State of the art in use of graphene in Li Sulphur batteries |

| 9.18. | Graphene battery announcement |

| 9.19. | Graphene-enabled products and important prototypes |

| 10. | COMPOSITES |

| 10.1. | General observation on using graphene additives in composites |

| 10.2. | Commercial results on graphene conductive composites |

| 10.3. | Conductive composites |

| 10.4. | EMI Shielding |

| 10.5. | How do CNTs do in conductive composites |

| 10.6. | CNT success in conductive composites |

| 10.7. | Examples of products that use CNTs in conductive plastics |

| 10.8. | Young's Modulus enhancement |

| 10.9. | Commercial results on permeation graphene improvement |

| 10.10. | Permeation Improvement |

| 10.11. | Thermal conductivity improvement |

| 10.12. | Commercial results on thermal conductivity improvement using graphene |

| 10.13. | Thermal conductivity improvement using graphene |

| 11. | GRAPHENE AND 2D MATERIALS FOR TRANSISTORS |

| 11.1. | Performance of graphene transistors |

| 11.2. | Graphene transistor based on work function modulation |

| 11.3. | Other 2D materials are better at creating transistor functions |

| 11.4. | Mobility of 2D materials as a function of bandgap |

| 11.5. | Suitability of 2D materials for large-area flexible devices |

| 11.6. | Effect of growth method on mobility |

| 12. | TIRES |

| 12.1. | Graphene as additive in tires |

| 12.2. | Progress on graphene-enabled bicycle tires |

| 12.3. | Carbon black in tires |

| 12.4. | Black carbon in car tires |

| 12.5. | There are many types of black carbon |

| 12.6. | CNT and graphene are the least ready emerging tech for tire improvement |

| 12.7. | Results on use of graphene in silica loaded tires |

| 12.8. | Comments on CNT and graphene in tires |

| 12.9. | Total addressable market for graphene in tires |

| 13. | SENSORS |

| 13.1. | Graphene GFET sensors |

| 13.2. | Fast graphene photosensor |

| 13.3. | Graphene humidity sensor |

| 13.4. | Optical brain sensors using graphene |

| 13.5. | Graphene skin electrodes |

| 13.6. | Wearable stretch sensor using graphene |

| 14. | OTHER APPLICATIONS |

| 14.1. | Anti-corrosion coating |

| 14.2. | Water filtration |

| 14.3. | Lockheed Martin's water filtration |

| 14.4. | Graphene-enhanced condoms? |

| 14.5. | Future applications |

| 15. | REVIEW OF PROGRESS WITH CARBON NANOTUBES |

| 15.1. | Carbon nanotubes- the big picture |

| 15.2. | Carbon nanotubes are more mature than graphene |

| 15.3. | Carbon nanotubes prices are falling |

| 15.4. | Already commercial applications of CNTs |

| 15.5. | Application Timeline |

| 15.6. | Production capacity of carbon nanotubes |

| 15.7. | Loss of differentiation in CNTs |

| 15.8. | Differentiating between CNTs and graphene |

| 15.9. | Will the CNT industry consolidate? |

| 15.10. | Player dynamics in the CNT business |

| 15.11. | Ten-year market forecast for MWCNTs |

| 16. | INTERVIEW BASED COMPANY PROFILES |

| 16.1. | Abalonyx AS |

| 16.2. | Advanced Graphene Products |

| 16.3. | Anderlab Technologies Pvt. Ltd. |

| 16.4. | Angstron Materials |

| 16.5. | Applied Graphene Materials |

| 16.6. | Arkema |

| 16.7. | AzTrong |

| 16.8. | Bayer MaterialScience AG (now left the business) |

| 16.9. | Bluestone Global Tech |

| 16.10. | C3Nano |

| 16.11. | Cabot Corporation |

| 16.12. | Cambridge Nanosystems |

| 16.13. | Canatu |

| 16.14. | Charmtron Inc |

| 16.15. | CNano Technology |

| 16.16. | CrayoNano |

| 16.17. | Directa Plus |

| 16.18. | g2o |

| 16.19. | Gnanomat |

| 16.20. | Grafen Chemical Industries |

| 16.21. | Grafentek |

| 16.22. | Grafoid |

| 16.23. | Graphenano |

| 16.24. | Graphene 3D Lab |

| 16.25. | Graphene Frontiers |

| 16.26. | Graphene Laboratories, Inc |

| 16.27. | Graphene Square |

| 16.28. | Graphene Technologies |

| 16.29. | Graphenea |

| 16.30. | Group NanoXplore Inc. |

| 16.31. | Grupo Antolin Ingenieria |

| 16.32. | Incubation Alliance |

| 16.33. | Jinan Moxi New Material Technology |

| 16.34. | Nanjing JCNANO Technology |

| 16.35. | Nanocyl |

| 16.36. | NanoInnova |

| 16.37. | NanoIntegris |

| 16.38. | Nantero |

| 16.39. | Nanomedical Diagnostics |

| 16.40. | OCSiAl |

| 16.41. | OneD Material LLC |

| 16.42. | Perpetuus Graphene |

| 16.43. | Poly-Ink |

| 16.44. | Pyrograf Products |

| 16.45. | Raymor Industries, Inc. |

| 16.46. | Showa Denko K.K |

| 16.47. | SiNode Systems |

| 16.48. | Skeleton Technologies |

| 16.49. | SouthWest NanoTechnologies, Inc. |

| 16.50. | The Sixth Element |

| 16.51. | Thomas Swan |

| 16.52. | Timesnano |

| 16.53. | Unidym Inc |

| 16.54. | Vorbeck Materials |

| 16.55. | Wuxi Graphene Film |

| 16.56. | XFNANO |

| 16.57. | XG Sciences, Inc. |

| 16.58. | Xiamen Knano |

| 16.59. | XinNano Materials Inc |

| 16.60. | Xolve, Inc |

| 16.61. | Zyvex |

| 17. | COMPANY PROFILES |

| 17.1. | 2D Carbon Graphene Material Co., Ltd |

| 17.2. | Airbus, France |

| 17.3. | Aixtron, Germany |

| 17.4. | AMO GmbH, Germany |

| 17.5. | Asbury Carbon, USA |

| 17.6. | AZ Electronics, Luxembourg |

| 17.7. | BASF, Germany |

| 17.8. | Cambridge Graphene Centre, UK |

| 17.9. | Cambridge Graphene Platform, UK |

| 17.10. | Carben Semicon Ltd, Russia |

| 17.11. | Carbon Solutions, Inc., USA |

| 17.12. | Catalyx Nanotech Inc. (CNI), USA |

| 17.13. | CRANN, Ireland |

| 17.14. | Georgia Tech Research Institute (GTRI), USA |

| 17.15. | Grafoid, Canada |

| 17.16. | Graphene Devices, USA |

| 17.17. | Graphene NanoChem, UK |

| 17.18. | Graphensic AB, Sweden |

| 17.19. | HDPlas, USA |

| 17.20. | Head, Austria |

| 17.21. | HRL Laboratories, USA |

| 17.22. | IBM, USA |

| 17.23. | iTrix, Japan |

| 17.24. | JiangSu GeRui Graphene Venture Capital Co., Ltd. |

| 17.25. | Lockheed Martin, USA |

| 17.26. | Massachusetts Institute of Technology (MIT), USA |

| 17.27. | Max Planck Institute for Solid State Research, Germany |

| 17.28. | Momentive, USA |

| 17.29. | Nanjing JCNANO Tech Co., LTD |

| 17.30. | Nanjing XFNANO Materials Tech Co.,Ltd |

| 17.31. | Nanostructured & Amorphous Materials, Inc., USA |

| 17.32. | Nokia, Finland |

| 17.33. | Pennsylvania State University, USA |

| 17.34. | Power Booster, China |

| 17.35. | Quantum Materials Corp, India |

| 17.36. | Rensselaer Polytechnic Institute (RPI), USA |

| 17.37. | Rice University, USA |

| 17.38. | Rutgers - The State University of New Jersey, USA |

| 17.39. | Samsung Electronics, Korea |

| 17.40. | Samsung Techwin, Korea |

| 17.41. | SolanPV, USA |

| 17.42. | Spirit Aerosystems, USA |

| 17.43. | Sungkyunkwan University Advanced Institute of Nano Technology (SAINT), Korea |

| 17.44. | Texas Instruments, USA |

| 17.45. | Thales, France |

| 17.46. | University of California Los Angeles, (UCLA), USA |

| 17.47. | University of Manchester, UK |

| 17.48. | University of Princeton, USA |

| 17.49. | University of Southern California (USC), USA |

| 17.50. | University of Texas at Austin, USA |

| 17.51. | University of Wisconsin-Madison, USA |

| IDTECHEX RESEARCH REPORTS AND CONSULTANCY |

Report Statistics

| Slides | 235 |

|---|---|

| Companies | 112 |

| Forecasts to | 2026 |

Customer Testimonial