Key Business Models for Electrolyzer Firms in Green Hydrogen Projects

May 17, 2024

Green hydrogen production utilizes four main electrolyzer technologies: alkaline water electrolysis (AWE), proton exchange membrane (PEM), anion exchange membrane (AEM), and solid oxide electrolyzers (SOEC). Each technology has its own operational principles, performance characteristics, and commercial maturity. These systems integrate with the balance of plant (BOP) components, including transformers, rectifiers, and purification systems, to produce hydrogen at the right pressure and purity.

Electrolyzer OEMs have adopted various business strategies to deploy their systems into commercial projects. This article shares some of the research from the IDTechEx report "Green Hydrogen Production & Electrolyzer Market 2024-2034: Technologies, Players, Forecasts", highlighting some of the main business models along with industry examples.

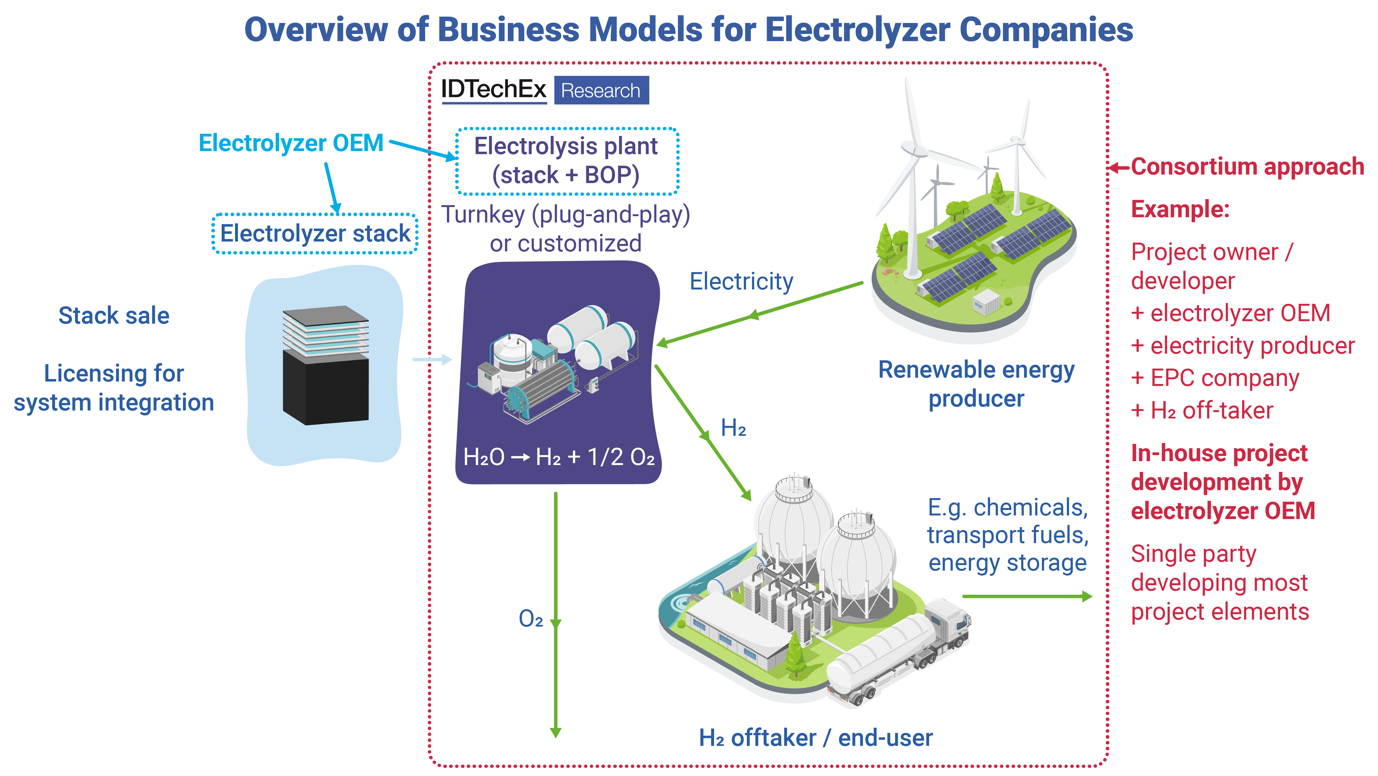

Overview of business models for electrolyzer companies. Source: IDTechEx

Licensing of electrolyzer stacks and use of system integration partners

New OEMs often choose to license their technology to concentrate on their core strengths - designing, enhancing, and manufacturing electrolyzer stacks. This strategy allows them to expand without the significant capital investment required to establish international offices and integrate BOP and commissioning projects. Licensing speeds up technology deployment and revenue generation but comes with risks like potential IP mismanagement and quality inconsistencies due to third-party integration.

Notable companies that license their stack technologies include Ceres Power (SOEC), Hoeller Electrolyzer (PEMEL), PERIC (AWE), and Enapter (AEMEL). Enapter exemplifies a relatively young company successfully adopting this business model. By building a network of distribution partners and system integrators, Enapter has managed to extend its reach quickly beyond European markets, demonstrating the effectiveness of licensing in facilitating rapid geographic and market expansion.

Turnkey solution providers (stack + BOP)

This model involves the OEM supplying both the electrolyzer stack and all necessary BOP components, often delivered in containerized or skid-mounted systems. It appeals to clients looking for a simplified procurement and installation process with a single point of contact for the entire system. This approach can significantly increase revenue per project and strengthen customer relationships. However, it requires substantial investment in design, assembly, and maintenance capabilities and carries risks related to project execution failures and supply chain disruptions related to the BOP.

A wide range of electrolyzer OEMs, including well-established players such as Nel, Plug Power, thyssenkrupp nucera, and ITM Power, opt for this approach as one of their revenue generation strategies. While all types of electrolyzers can be configured into turnkey systems, it is more common among PEM electrolyzer OEMs. This preference is due to the superior dynamic ramping capabilities of PEM systems, which are advantageous for renewable energy storage and smaller, more modular applications like hydrogen refueling stations. In contrast, AWE OEMs often provide more customized systems that cater to specific client needs and larger-scale applications.

Customized systems for projects

OEMs also provide customized systems where the electrolyzer stack and BOP are designed to meet specific project requirements, optimizing overall system efficiency and performance. This bespoke approach caters to clients needing systems tailored to large-scale industrial applications or integration with existing infrastructure. However, customized systems require extensive engineering expertise and manage complexities in project development, potentially extending timelines.

Many of the same OEMs that provide turnkey solutions also offer customized systems. These companies recognize the dual benefits of being able to cater to a broader range of market needs - from standardized turnkey solutions for quicker deployment to highly customized systems that optimize performance for specific applications. By offering both, these OEMs can accommodate a wider array of client requirements, ensuring flexibility and adaptability in their service offerings.

Consortium approaches in project development

Electrolyzer OEMs often participate in consortiums developing projects. This involves multiple entities, including possibly competing firms, collaborating to share the risks and rewards of large-scale projects. This strategy allows for pooling of expertise and financial resources, reducing the burden on any single company and potentially allowing projects on a scale that would be difficult to achieve alone. This is particularly suitable for large complex projects with multiple end-users that are often aiming to demonstrate a concept. The main disadvantages are potential differences in corporate processes leading to slower decision-making and complexities in aligning different technical approaches.

In-house project development by electrolyzer OEMs

OEMs that develop projects on their own take full responsibility for every aspect of the project. This includes technology development and manufacturing, as well as contracting EPC companies, securing long-term offtakers, financing the project, and overseeing commissioning and operations. This model allows for maximal control over the value chain, which can lead to higher margins and a direct relationship with end-users. It is particularly suited to large companies with robust financial backing and extensive expertise across multiple domains. However, the primary challenges include substantial capital requirements, the management of various project elements, and the full assumption of operational and market risks.

Plug Power is as a notable example of a pure-play hydrogen equipment company that adopts this in-house project development approach. The company is developing multiple liquid hydrogen production sites across the US, managing all project elements from production to the delivery of liquid hydrogen to its customers. Despite its pioneering efforts, Plug Power is facing financial challenges as it bears most of the project risks on its own. 2023 and 2024 financial reports indicate a significant increase in quarterly losses amid a drop in revenue as the company awaits the commissioning of several of its PEM electrolyzer systems and a new pricing regime to take effect. These financial strains underscore the inherent risks of this business model, especially when transitioning to larger product scales and managing upfront costs. Nevertheless, Plug Power expects to see an improvement in its performance in the second half of 2024.

Technology-specific narratives and further insights

AEM electrolyzers, typically used in small-scale applications, are less mature compared to PEM and AWE technologies, with significant developments now pushing into medium-scale capacities. PEM electrolyzers, recognized for their operational reliability, are commonly deployed in applications ranging from small to medium scales, with current project capacities under 50 MW. Though PEM technology is mature, larger projects over 100 MW are still in the development stages. Alkaline water electrolysis (AWE), the most mature technology, is employed widely across small to large-scale projects over 100 MW, including emerging GW-scale projects. Solid oxide electrolyzers (SOEC), which operate at high temperatures, are optimal for integration with industrial processes that can provide necessary heat or steam, facilitating highly efficient operations and allowing for innovative applications such as synthetic fuel production by co-electrolysis of CO2 and H2O.

The IDTechEx report "Green Hydrogen Production & Electrolyzer Market 2024-2034: Technologies, Players, Forecasts" provides further discussions and commercial examples of electrolyzer firms' efforts. The report also provides 10-year market forecasts in gigawatts (GW) of electrolyzer capacity and US$ billions (US$B) for the key electrolyzer technologies, discussion of novel electrolysis technologies (e.g., seawater & CO2 electrolysis), comprehensive analysis of electrolyzer manufacturers by state of development and system specifications, analysis of manufacturing capacities by technology and region, green hydrogen project case studies as well as outlooks on future electrolyzer technology adoption.

To find out more about this report, including downloadable sample pages, please visit www.IDTechEx.com/Electrolyzer.

For the full portfolio of hydrogen market research from IDTechEx, please see www.IDTechEx.com/Research/Hydrogen.

IDTechEx provides trusted independent research on emerging technologies and their markets. Since 1999, we have been helping our clients to understand new technologies, their supply chains, market requirements, opportunities and forecasts. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.