Fuel Cell Boats & Ships, a Methanol to the Madness

Mar 07, 2023

IDTechEx has published a series of articles recently covering hydrogen- and ammonia-powered fuel cell (FC) demand in shipping. One of the most common responses to this has been - what about methanol?

Indeed, methanol has garnered lots of interest, particularly since shipping giant Maersk ordered 19 methanol (combustion) ships, with deliveries beginning in 2025. This article evaluates methanol versus the alternatives and speculates on its potential future adoption in the marine industry.

For more on IDTechEx's granular outlook on fuel cell use in the maritime sector, see the new IDTechEx report, "Fuel Cell Boats & Ships 2023-2033: PEMFC, SOFC, Hydrogen, Ammonia, LNG".

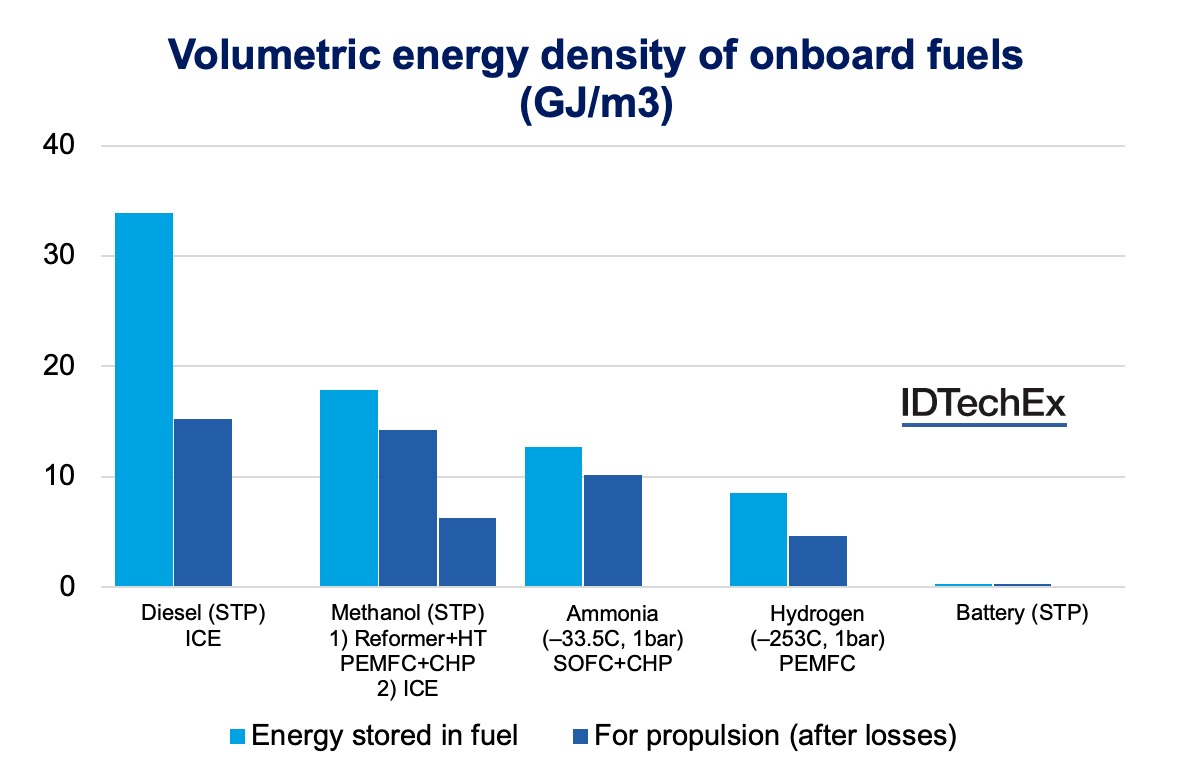

Green methanol is one of the most comparable alternative fuels to diesel in terms of energy density. And since methanol can be transported as a liquid at around ambient conditions, existing diesel bunker infrastructure can be modified for methanol rapidly at low cost, in contrast to liquid hydrogen and ammonia which require much lower liquefaction temperatures (-253C and -33C, respectively). These advantages make the logistics of using methanol easy, making it attractive for ship operators.

Volumetric energy density of onboard fuels (GJ/m3). Source: IDTechEx

Volumetric energy density of onboard fuels (GJ/m3). Source: IDTechExMethanol will first enter the market via combustion engines, but around the corner is high temperature (HT) PEMFCs, where several companies are advancing rapidly. HT PEMFCs are advantageous as they allow low-purity hydrogen to be used, such as syngas. This means the system can be combined with a simple methanol reformer, one which does not require exotic and expensive membrane materials. In contrast, low-temperature (LT) PEMFCs are highly sensitive and require hydrogen at over 99.99% purity. A methanol reformer feeding a HT PEMFC can result in over 50% efficiency, compared to around 35% in a methanol combustion engine. With combined heat and power (CHP) processes, there is potential for fuel cells to rise above 80% efficiency. Blue World Technologies, from Denmark, and Boston-based Advent Technologies are exciting companies which have proven the concept. Advent was recently awarded around 782 million euros from the EU's IPCEI project to build 400MW of capacity in Greece by 2027.

There are, however, many disadvantages to methanol. Green methanol is still a hydrocarbon, and its use can only sustain current carbon levels since it re-emits the carbon captured to make it. This undermines its potential as a long-term solution compared to green hydrogen and ammonia, particularly as the IMO shifts focus towards regulating greenhouse gases. Nonetheless, high concentrations of CO2 are created as a by-product in methanol systems, which lends itself to (re) carbon capture. This creates the potential for a more 'circular' approach which would keep carbon out of the environment, although this is currently a secondary priority for suppliers and adds cost and complexity.

Another factor important in the midterm is that green methanol is still a derivative of green hydrogen. For the next decade, green hydrogen will be in short supply, expensive, and demanded by multiple sectors for the so-called hydrogen economy - funneling it into first-use applications will be the most efficient way to lower emissions. For more information, IDTechEx's latest hydrogen production forecasts can be found in the reports "Green Hydrogen Production: Electrolyzer Markets 2023-2033" and "Blue Hydrogen Production and Markets 2023-2033: Technologies, Forecasts, Players".

The industry must also factor in the continued use of LNG or methane. While LNG emits powerful greenhouse gases with methane slip, the fuel has a similar performance to methanol and can also be created artificially with green hydrogen and carbon capture (e-methane). While the bunker infrastructure for liquid methane is costly (due to the -153C storage requirement), it has been growing for decades due to initial regulation focused on reducing emissions of SOx, NOx, and PM, which it does well.

The question becomes: is it worth dividing resources to develop LNG/methane, ammonia and hydrogen, and methanol? Choosing to develop a few promising solutions quickly, rather than everything everywhere all at once, would be wise. Hydrogen and ammonia create a long-term pathway to zero GHG emissions. Between the hydrocarbons, LNG has a similar performance to methanol and is already widely developed today. Moreover, the continued importance and demand for LNG carriers were indeed highlighted in 2022 with the disruption to natural gas pipelines.

As stated earlier in this series, overall, it is easy to envisage a future with broader adoption of hydrogen PEMFC and batteries in the mid-term and ammonia SOFC adoption in the long term for a true pathway to zero emissions. However, the slow development of these solutions could create opportunities for methanol. What is clear is that decarbonizing the marine industry is an immense challenge and one which will continue to rely on multiple solutions, investments, new regulations, collaboration, and testing from both the public and private sectors.

IDTechEx Research

This research forms part of the broader electric vehicle and energy storage portfolio from IDTechEx, who track electric vehicle markets and technologies across land, sea and air, helping you navigate whatever may be ahead. Find out more at www.IDTechEx.com/Research/EV.