Three Reasons Why Autonomy Will Boost Automotive Semiconductor Markets

Feb 20, 2023

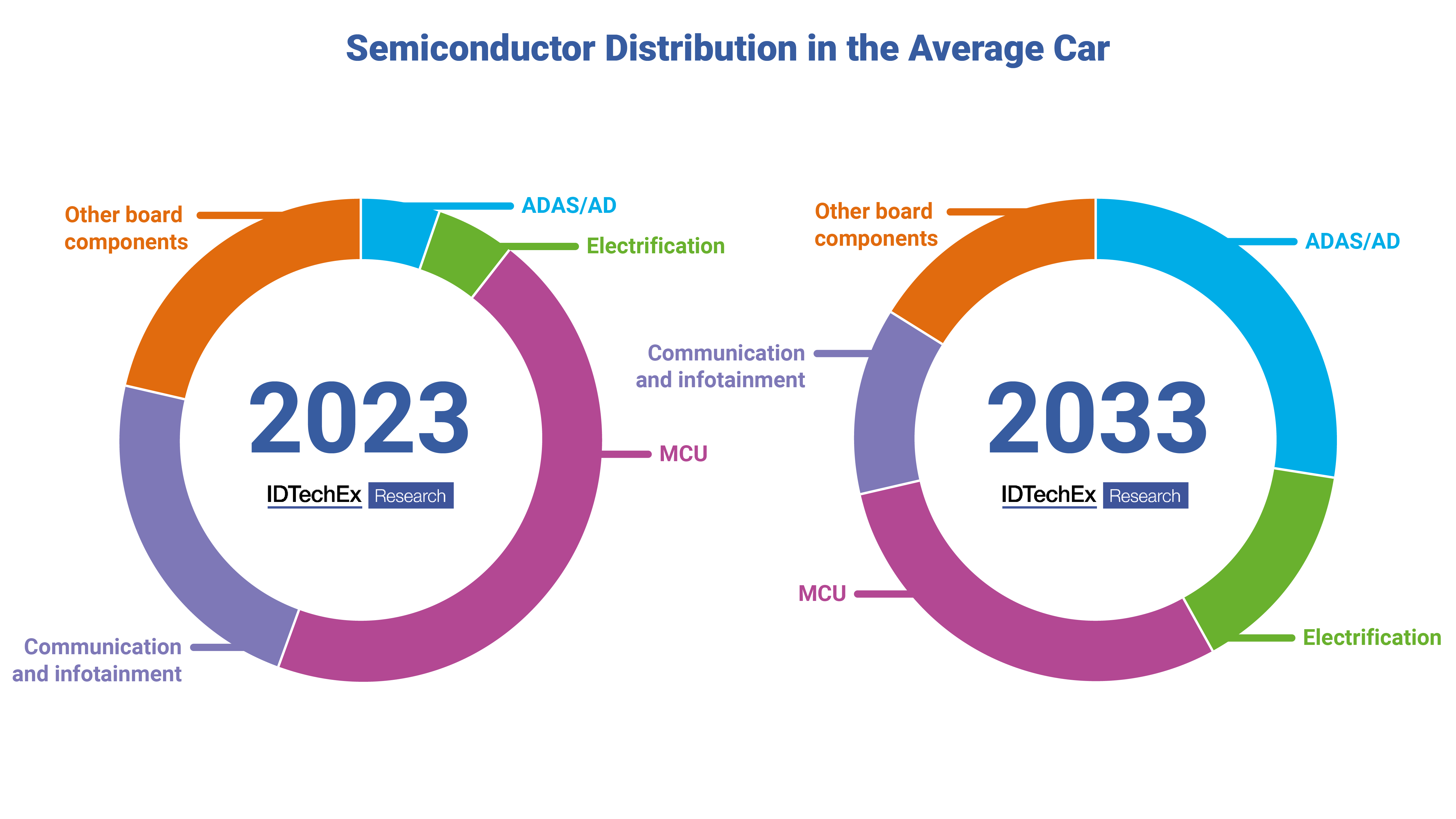

IDTechEx's new "Automotive Semiconductors 2023-2033" report provides a deep dive into the existing and emerging semiconductor technologies used in vehicles today and tomorrow. The report focuses on the areas of automation and electrification, explaining what semiconductor technologies are needed and how their growth is going to drive a 10-year CAGR of 9.4% in the automotive semiconductor market. However, semiconductors for automation will grow even faster. IDTechEx's research finds that semiconductors for ADAS (advanced driver assistance systems) and autonomy will grow at a 10-year CAGR of 29%. As such, autonomy will be a boon for the automotive semiconductor industry and here are three reasons for that growth.

ADAS/AD are the largest growing semiconductor applications in vehicles. Source: IDTechEx - "Automotive Semiconductors 2023-2033"

Automated Vehicles Are Coming

This might even be an understatement. The industry has been guilty of saying that autonomous vehicles are just around the corner for some time, but in some ways, they are already here. Just last month, the Mercedes S-Class got SAE level 3 certification in the US, following its certification in Germany in 2022. This has huge significance as the S-Class tends to be the trendsetter in the automotive industry, and IDTechEx is confident that level 3 technologies will trickle down through vehicle price points over the next decade. Even level 4 vehicles now have an established presence in some cities. In Phoenix, Arizona, anyone can use Waymo's completely driverless robotaxis, providing the route and end destination is within select geofenced regions. Autonomous vehicles are not coming; they are here and bring more sensors, more computers, and more semiconductor demand.

More Sensors Using More Advanced Technologies

Not only will autonomous vehicles bring more sensors to vehicles, but they will also require higher-performing sensors with more expensive and more advanced semiconductor technologies. Radar, for example, has previously used quite mature 90nm SiGe BiCMOS technologies, but demand for better performance means that the next generation, 4D imaging radars will be adopting Si CMOS technologies with nodes of 40nm and less. As the node size drops, these radars gain performance, but they will also be gaining cost.

LiDAR has been coming down in price recently, and its adoption is growing. It is a key sensor for vehicles at SAE level 3 and above, but due to the safety benefits it can bring, IDTechEx thinks it will also begin penetrating level 2 and below. Near-infrared LiDARs are the most deployed at the moment, and their detectors can be built on Silicon, making them quite cheap. But IDTechEx's "Automotive Semiconductors 2023-2033" report finds that the trend in LiDAR is towards shortwave infrared, which brings performance advantages but requires more expensive InGaAs detectors. IDTechEx sees their increased adoption and transition towards higher value semiconductor types as key drivers in the semiconductor for autonomy and ADAS markets.

High-Performance Computing - Driving Vehicles and Driving the Semiconductor Market

Finally, these highly automated vehicles are going to require high-performance computers capable of thousands of TOPs (tera-operations per second). The chips inside these computers are made using some of the most advanced processes by leading semiconductor foundries like TSMC and Samsung. This will also impact the automotive semiconductor supply chain; previously, microcontrollers (MCUs) have been the main computers in cars, built on mature technology nodes by established tier 2 suppliers such as Infineon and NXP. But the high-performance computing is beyond their internal fabrication capability, so they outsource to the East Asian giants. But others can do this as well, which is why fabless companies like Mobileye and Nvidia can get more of a stake in the automotive semiconductor market.

The vehicles of tomorrow are going to be more advance and demand more advancements from the semiconductor industry; find out exactly how in IDTechEx's "Automotive Semiconductors 2023-2033" report. It is fair to say then that autonomy will not just be driving individuals; it will be driving the entire automotive semiconductor industry.

IDTechEx Mobility Research

IDTechEx is actively researching autonomy and electrification and has just released a new report, "Automotive Semiconductors 2023-2033". To find out more, including downloadable sample pages, please visit www.IDTechEx.com/AutoSemi.

This research forms part of the broader mobility research portfolio from IDTechEx, who track the adoption of autonomy, electric vehicles, automotive semiconductors, battery trends, and demand across land, sea and air, helping to navigate whatever may be ahead. Find out more at www.IDTechEx.com/Research/EV.

Upcoming Free-to-Attend Webinar

How Autonomy Will Shake-up the Automotive Semiconductor Supply Chain

Dr James Jeffs, Senior Technology Analyst at IDTechEx and author of this article, will be presenting a webinar on the topic on Thursday 16 March 2023 - "How Autonomy Will Shake-up the Automotive Semiconductor Supply Chain".

Semiconductor technologies have been present in vehicles since the 1960s, first introduced for safety features such as stability control. Back then, and until recently, vehicles have been defined by performance characteristics such as engine power, handling, efficiency and so on. Semiconductor technologies developed with the vehicle, but even into the 21st century, the focus has been on those engine characteristics.

Change is happening. With the rise of electrification and automation, engine centricity is being replaced with a focus on software-oriented features like autonomous driving. These require much more powerful computers than have previously been used in vehicles. The chips for these systems are increasingly beyond the fabrication capabilities of the established tier 2 suppliers.

This webinar will:

- Explain the main areas which rely on semiconductor technologies in modern vehicles

- Discuss how automation and electrification trends will impact semiconductor demand

- Show the current capabilities of automotive tier 2 companies

- Examine how the supply chain is shifting to accommodate more high-performance computing in vehicles

Click here to find out more and register your place on one of our three sessions.