This report has been updated. Click here to view latest edition.

If you have previously purchased the archived report below then please use the download links on the right to download the files.

Solid-State and Polymer Batteries 2020-2030: Technology, Patents, Forecasts, Players

Revolutionary approach for the battery business

| 1. | EXECUTIVE SUMMARY AND CONCLUSIONS |

| 1.1. | Players discussed in this report |

| 1.2. | Status and future of solid-state battery business |

| 1.3. | Regional efforts: Germany, France, UK, Australia, USA, Japan, Korea and China |

| 1.4. | Location overview of major solid-state battery companies |

| 1.5. | Solid-state battery partner relationships |

| 1.6. | Solid-state electrolyte technology approach |

| 1.7. | Summary of solid-state electrolyte technology |

| 1.8. | Comparison of solid-state electrolyte systems |

| 1.9. | Technology evaluation |

| 1.10. | Technology evaluation: polymer vs. LLZO vs. LATP vs. LGPS |

| 1.11. | Technology and manufacturing readiness |

| 1.12. | Score comparison |

| 1.13. | Solid state battery collaborations / acquisitions by OEMs |

| 1.14. | Battery ambitions |

| 1.15. | Solid-state battery value chain |

| 1.16. | Potential applications for solid-state batteries |

| 1.17. | Market readiness |

| 1.18. | Solid-state batteries for electric vehicles |

| 1.19. | Solid-state batteries for consumer electronics |

| 1.20. | Performance comparison: Electric Vehicles |

| 1.21. | Performance comparison: CEs & wearables |

| 1.22. | Market forecast methodology |

| 1.23. | Assumptions and analysis of market forecast of SSB |

| 1.24. | Price forecast of solid-state battery for various applications |

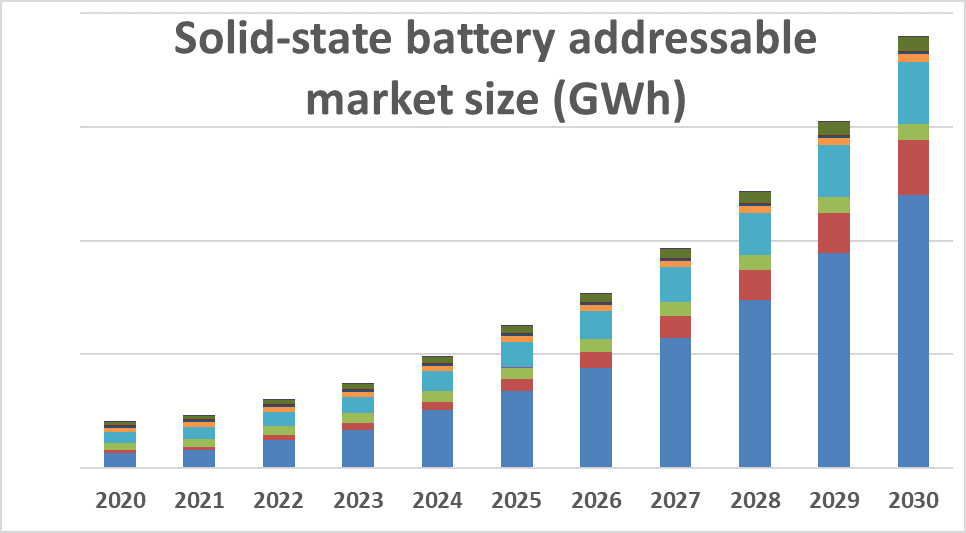

| 1.25. | Solid-state battery addressable market size |

| 1.26. | Solid-state battery forecast 2020-2030 by application |

| 1.27. | Market size segmentation in 2025 and 2030 |

| 1.28. | Solid-state battery forecast 2020-2030 by technology |

| 1.29. | Solid-state battery forecast 2020-2030 for car plug in |

| 2. | BACKGROUND |

| 2.1.1. | Introduction |

| 2.2. | Why Is Battery Development so Slow? |

| 2.2.1. | What is a battery? |

| 2.2.2. | A big obstacle — energy density |

| 2.2.3. | Battery technology is based on redox reactions |

| 2.2.4. | Electrochemical reaction is essentially based on electron transfer |

| 2.2.5. | Electrochemical inactive components reduce energy density |

| 2.2.6. | The importance of an electrolyte in a battery |

| 2.2.7. | Cathode & anode need to have structural order |

| 2.2.8. | Failure story about metallic lithium anode |

| 2.3. | Safety Issues with Lithium-Ion Batteries |

| 2.3.1. | Safety of liquid-electrolyte lithium-ion batteries |

| 2.3.2. | Modern horror films are finding their scares in dead phone batteries |

| 2.3.3. | Samsung's Firegate |

| 2.3.4. | Safety aspects of Li-ion batteries |

| 2.3.5. | LIB cell temperature and likely outcome |

| 2.4. | Li-ion Batteries |

| 2.4.1. | Food is electricity for humans |

| 2.4.2. | What is a Li-ion battery (LIB)? |

| 2.4.3. | Anode alternatives: Lithium titanium and lithium metal |

| 2.4.4. | Anode alternatives: Other carbon materials |

| 2.4.5. | Anode alternatives: Silicon, tin and alloying materials |

| 2.4.6. | Cathode alternatives: LNMO, NMC, NCA and Vanadium pentoxide |

| 2.4.7. | Cathode alternatives: LFP |

| 2.4.8. | Cathode alternatives: Sulphur |

| 2.4.9. | Cathode alternatives: Oxygen |

| 2.4.10. | High energy cathodes require fluorinated electrolytes |

| 2.4.11. | Why is lithium so important? |

| 2.4.12. | Where is lithium? |

| 2.4.13. | How to produce lithium |

| 2.4.14. | Where is lithium used |

| 2.4.15. | Question: how much lithium do we need? |

| 2.4.16. | How can LIBs be improved? |

| 2.5. | Battery Requirement |

| 2.5.1. | Push and pull factors in Li-ion research |

| 2.5.2. | The battery trilemma |

| 2.5.3. | Performance limit |

| 2.5.4. | Form factor |

| 2.5.5. | Cost |

| 2.6. | Conclusions |

| 2.6.1. | Conclusions |

| 3. | LONGING FOR ALL SOLID-STATE BATTERIES |

| 3.1. | Why Solid-State Batteries? |

| 3.1.1. | A solid future? |

| 3.1.2. | Lithium-ion batteries vs. solid-state batteries |

| 3.1.3. | What is a solid-state battery (SSB)? |

| 3.1.4. | How can solid-state batteries increase performance? |

| 3.1.5. | Close stacking |

| 3.1.6. | Energy density improvement |

| 3.1.7. | Value propositions and limitations of solid-state battery |

| 3.1.8. | Flexibility and customisation provided by solid-state batteries |

| 3.2. | Interests on Solid-State Batteries |

| 3.2.1. | Research efforts on solid-state batteries |

| 3.2.2. | A new cycle of interests |

| 3.2.3. | Interests in China |

| 3.2.4. | CATL |

| 3.2.5. | Qing Tao Energy Development |

| 3.2.6. | History of Qing Tao Energy Development |

| 3.2.7. | Ganfeng Lithium |

| 3.2.8. | Ningbo Institute of Materials Technology & Engineering, CAS |

| 3.2.9. | WeLion New Energy Technology |

| 3.2.10. | JiaWei Renewable Energy |

| 3.2.11. | 15 Other Chinese player activities on solid state batteries |

| 3.2.12. | Enovate Motors |

| 3.2.13. | Chinese car player activities on solid-state batteries |

| 3.2.14. | Regional interests: Japan |

| 3.2.15. | Technology roadmap according to Germany's NPE |

| 3.2.16. | Roadmap for battery cell technology |

| 3.2.17. | SSB project - Ionics |

| 3.2.18. | SSB project - SBIR 2016 |

| 3.2.19. | Automakers' efforts - BMW |

| 3.2.20. | Automakers' efforts - Volkswagen |

| 3.2.21. | Automakers' efforts - Hyundai |

| 3.2.22. | Automakers' efforts - Toyota |

| 3.2.23. | Automakers' efforts - Fisker Inc. |

| 3.2.24. | Automakers' efforts - Bolloré |

| 3.2.25. | Battery vendors' efforts - Panasonic |

| 3.2.26. | Battery vendors' efforts - Samsung SDI |

| 3.2.27. | Academic views - University of Münster |

| 3.2.28. | Academic views - Giessen University |

| 3.2.29. | Academic views - Fraunhofer Batterien |

| 4. | SOLID-STATE BATTERIES |

| 4.1. | Introduction to Solid-State Batteries |

| 4.1.1. | History of solid-state batteries |

| 4.1.2. | Solid-state battery configurations |

| 4.1.3. | Solid-state electrolytes |

| 4.1.4. | Differences between liquid and solid electrolytes |

| 4.1.5. | How to design a good solid-state electrolyte |

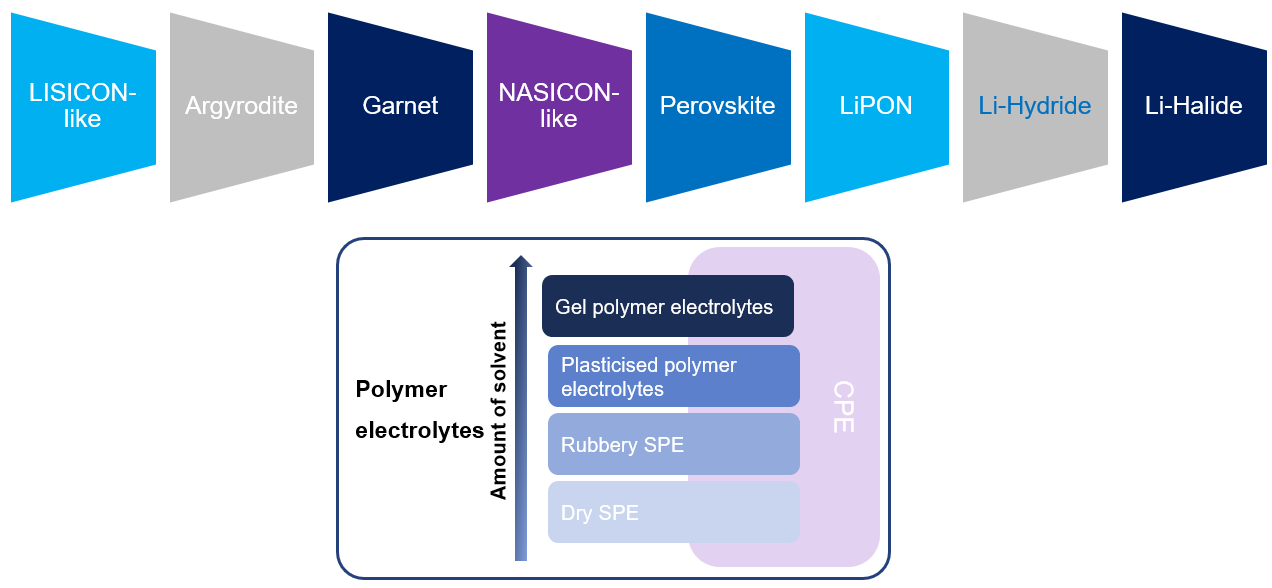

| 4.1.6. | Classifications of solid-state electrolyte |

| 4.1.7. | Thin film vs. bulk solid-state batteries |

| 4.1.8. | Scaling of thin ceramic sheets |

| 4.1.9. | How safe are solid-state batteries? |

| 4.2. | Solid Polymer Electrolytes |

| 4.2.1. | Applications of polymer-based batteries |

| 4.2.2. | LiPo batteries, polymer-based batteries, polymeric batteries |

| 4.2.3. | Types of polymer electrolytes |

| 4.2.4. | Electrolytic polymer options |

| 4.2.5. | Advantages and issues of polymer electrolytes |

| 4.2.6. | PEO for solid polymer electrolyte |

| 4.2.7. | Polymer-based battery: Solidenergy |

| 4.2.8. | Coslight |

| 4.2.9. | BrightVolt batteries |

| 4.2.10. | BrightVolt product matrix |

| 4.2.11. | BrightVolt electrolyte |

| 4.2.12. | Hydro-Québec |

| 4.2.13. | Solvay |

| 4.2.14. | IMEC |

| 4.2.15. | Polyplus |

| 4.2.16. | SEEO |

| 4.2.17. | Innovative electrode for semi-solid electrolyte batteries |

| 4.2.18. | Redefining manufacturing process by 24M |

| 4.2.19. | Ionic Materials |

| 4.2.20. | Technology and manufacturing process of Ionic Materials |

| 4.2.21. | Prieto Battery |

| 4.2.22. | Companies working on polymer solid state batteries |

| 4.3. | Solid Inorganic Electrolytes |

| 4.3.1. | Types of solid inorganic electrolytes for Li-ion |

| 4.3.2. | Oxide Inorganic Electrolyte |

| 4.3.3. | Oxide electrolyte |

| 4.3.4. | Garnet |

| 4.3.5. | QuantumScape's technology |

| 4.3.6. | Karlsruhe Institute of Technology |

| 4.3.7. | Nagoya University |

| 4.3.8. | Toshiba |

| 4.3.9. | NASICON-type |

| 4.3.10. | Lithium ion conducting glass-ceramic powder-01 |

| 4.3.11. | LICGCTM PW-01 for cathode additives |

| 4.3.12. | Ohara's products for solid state batteries |

| 4.3.13. | Ohara / PolyPlus |

| 4.3.14. | Application of LICGC for all solid-state batteries |

| 4.3.15. | Properties of multilayer all solid-state lithium ion battery using LICGC as electrolyte |

| 4.3.16. | LICGC products at the show |

| 4.3.17. | Manufacturing process of Ohara glass |

| 4.3.18. | Taiyo Yuden |

| 4.3.19. | Schott |

| 4.3.20. | Perovskite |

| 4.3.21. | LiPON |

| 4.3.22. | LiPON: construction |

| 4.3.23. | Players worked and working LiPON-based batteries |

| 4.3.24. | Cathode material options for LiPON-based batteries |

| 4.3.25. | Anodes for LiPON-based batteries |

| 4.3.26. | Substrate options for LiPON-based batteries |

| 4.3.27. | Trend of materials and processes of thin-film battery in different companies |

| 4.3.28. | LiPON: capacity increase |

| 4.3.29. | Technology of Infinite Power Solutions |

| 4.3.30. | Cost comparison between a standard prismatic battery and IPS' battery |

| 4.3.31. | Thin-film solid-state batteries made by Excellatron |

| 4.3.32. | Johnson Battery Technologies |

| 4.3.33. | JBT's advanced technology performance |

| 4.3.34. | Ultra-thin micro-battery—NanoEnergy® |

| 4.3.35. | Micro-Batteries suitable for integration |

| 4.3.36. | From limited to mass production - STMicroelectronics |

| 4.3.37. | Summary of the EnFilm™ rechargeable thin-film battery |

| 4.3.38. | CEA Tech |

| 4.3.39. | Ilika |

| 4.3.40. | TDK |

| 4.3.41. | CeraCharge's performance |

| 4.3.42. | Main applications of CeraCharge |

| 4.3.43. | ProLogium: Solid-state lithium ceramic battery |

| 4.3.44. | ProLogium: "MAB" EV battery pack assembly |

| 4.3.45. | FDK |

| 4.3.46. | Applications of FDK's solid state battery |

| 4.3.47. | Companies working on oxide solid state batteries |

| 4.3.48. | Sulphide Inorganic Electrolyte |

| 4.3.49. | Solid Power |

| 4.3.50. | LISICON-type |

| 4.3.51. | Hitachi Zosen's solid-state electrolyte |

| 4.3.52. | Hitachi Zosen's batteries |

| 4.3.53. | Solid-state electrolytes - Konan University |

| 4.3.54. | Tokyo Institute of Technology |

| 4.3.55. | Argyrodite |

| 4.3.56. | Samsung's work with argyrodite |

| 4.3.57. | Companies working on sulphide solid state batteries |

| 4.3.58. | Others |

| 4.3.59. | Li-hydrides |

| 4.3.60. | Li-halides |

| 4.3.61. | Summary |

| 4.3.62. | Advantages and issues with inorganic electrolytes |

| 4.3.63. | Dendrites - ceramic fillers and high shear modulus are needed |

| 4.3.64. | Comparison between inorganic and polymer electrolytes |

| 4.4. | Patent Analysis around Solid-State Electrolytes |

| 4.4.1. | Overview of investigation |

| 4.4.2. | Total number of patents by electrolyte type and material |

| 4.4.3. | The SSE patent portfolio of key assignees |

| 4.5. | Patent Analysis on Non-Composite Inorganic or Polymeric Solid-State Electrolyte |

| 4.5.1. | Total number of patents by SSE material |

| 4.5.2. | Patent application fluctuations from 2014 to 2016 |

| 4.5.3. | Legal status of patents in 2018 by SSE material |

| 4.5.4. | Key assignee's patent portfolio of non-composite SSEs |

| 4.5.5. | PEO: Patent Activity Trends |

| 4.5.6. | LPS: Patent Activity Trends |

| 4.5.7. | LLZO: Patent Activity Trends |

| 4.5.8. | LLTO: Patent Activity Trends |

| 4.5.9. | Lithium Iodide: Patent Activity Trends |

| 4.5.10. | LGPS: Patent Activity Trends |

| 4.5.11. | LIPON: Patent Activity Trends |

| 4.5.12. | LATP: Patent Activity Trends |

| 4.5.13. | LAGP: Patent Activity |

| 4.5.14. | Argyrodite: Patent Activity Trends |

| 4.5.15. | LiBH4: Patent Activity Trends |

| 4.5.16. | Conclusions |

| 4.6. | Composite Electrolytes |

| 4.6.1. | The best of both worlds? |

| 4.6.2. | Toshiba |

| 4.7. | Solid-State Electrolytes Beyond Li-ion |

| 4.7.1. | Solid-state electrolytes in lithium-sulphur batteries |

| 4.7.2. | Lithium sulphur solid electrode development phases |

| 4.7.3. | Solid-state electrolytes in lithium-air batteries |

| 4.7.4. | Solid-state electrolytes in metal-air batteries |

| 4.7.5. | Solid-state electrolytes in sodium-ion batteries |

| 4.7.6. | Solid-state electrolytes in sodium-sulphur batteries |

| 5. | SOLID-STATE BATTERY MANUFACTURING |

| 5.1. | The real bottleneck |

| 5.2. | The incumbent process: lamination |

| 5.3. | Summary of processing routes of solid-state battery components fabrication |

| 5.4. | Process chains for solid electrolyte fabrication |

| 5.5. | Process chains for anode fabrication |

| 5.6. | Process chains for cathode fabrication |

| 5.7. | Process chains for cell assembly |

| 5.8. | Solid battery fabrication process |

| 5.9. | Manufacturing equipment for solid-state batteries |

| 5.10. | Typical manufacturing method of the all solid-state battery (SMD type) |

| 5.11. | Are thin film electrolytes viable? |

| 5.12. | Summary of main fabrication technique for thin film batteries |

| 5.13. | PVD processes for thin-film batteries |

| 5.14. | Ilika's PVD approach |

| 5.15. | Avenues for manufacturing |

| 5.16. | Toyota's approach |

| 5.17. | Hitachi Zosen's approach |

| 5.18. | Sakti3's PVD approach |

| 5.19. | Planar Energy's approach |

| 6. | COMPANY PROFILES |

| 6.1. | 24M |

| 6.2. | Ampcera |

| 6.3. | Blue Solutions |

| 6.4. | BrightVolt |

| 6.5. | Cymbet |

| 6.6. | EMPA |

| 6.7. | Flashcharge |

| 6.8. | FDK Corporation |

| 6.9. | Hitachi |

| 6.10. | Ilika |

| 6.11. | Ionic Materials |

| 6.12. | Johnson Battery Technologies |

| 6.13. | Kalptree Energy |

| 6.14. | Ohara |

| 6.15. | Planar Energy Devices |

| 6.16. | Polyplus Battery Company |

| 6.17. | Prieto Battery Inc. |

| 6.18. | ProLogium |

| 6.19. | QuantumScape |

| 6.20. | Sakti3 |

| 6.21. | SolidEnergy |

| 6.22. | Solid Power |

| 6.23. | Solvay |

| 6.24. | STMicroelectronics |

| 6.25. | Thin Film Electronics ASA |

| 6.26. | Toshiba |

| 6.27. | Toyota Central Research & Development Laboratories, Inc. |

| 7. | APPENDIX |

| 7.1. | Glossary of terms - specifications |

| 7.2. | Useful charts for performance comparison |

| 7.3. | Battery categories |

| 7.4. | Commercial battery packaging technologies |

| 7.5. | Comparison of commercial battery packaging technologies |

| 7.6. | Actors along the value chain for energy storage |

| 7.7. | Primary battery chemistries and common applications |

| 7.8. | Numerical specifications of popular rechargeable battery chemistries |

| 7.9. | Battery technology benchmark |

| 7.10. | What does 1 kilowatthour (kWh) look like? |

| 7.11. | Technology and manufacturing readiness |

| 7.12. | List of acronyms |

Report Statistics

| Slides | 336 |

|---|---|

| Forecasts to | 2030 |

Customer Testimonial