LiDAR On Its Way Out? Camera's Market Size From 76% to 79% by 2033

2023年3月15天

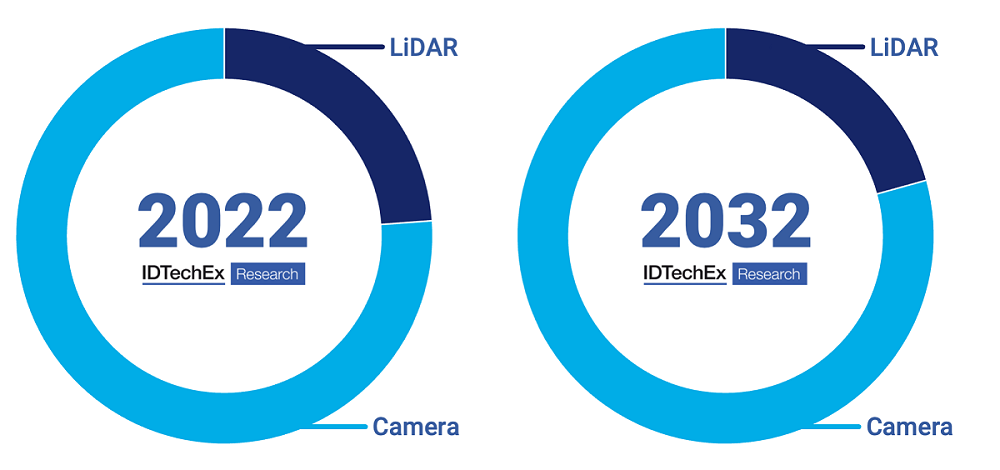

Autonomous mobility is the key value proposition for many robots. Thanks to the successes of self-driving systems in commercial vehicles from companies like Tesla and John Deere. Autonomous driving has gained significant momentum across the robotics industry. Autonomous driving for robots is nothing new, and autonomous mobility has traditionally heavily relied on LiDAR, thanks to their simplicity and ease of use. However, LiDAR presents a number of limitations, such as high upfront costs, low resolution, and lack of object recognition ability. With the recent successes of Tesla and John Deere's autonomous vehicles using cameras only, the tide is shifting, and cameras are poised to take over. IDTechEx's recent research, "Sensors for Robotics 2023-2043: Technologies, Markets, and Forecasts", shows that the market share of LiDAR in the robotics industry will decrease from 24% to 21%, whereas the market share of cameras is expected to increase by 3% over the next decade, as shown in the diagram below.

Market Share of LiDAR Units and Camera Units 2022 Versus 2032. Source: IDTechEx - "Sensors for Robotics 2023-2043: Technologies, Markets, and Forecasts"

In this article, IDTechEx Technology Analyst Yulin Wang will explore why cameras are becoming a more popular choice for mobile robots, what advantages they offer over LiDAR, as well as what limitations are holding them back from being adopted.

- 3D LiDAR is not needed for indoor mobile robots. One of the benefits of LiDAR is that they are less susceptible to poor weather conditions and limited visibility compared with cameras. While this is a significant benefit for outdoor robots that work in unpredictable weather, it is not quite needed for indoor mobile robots because they are fundamentally designed to work in a well-controlled environment with stable artificial illumination. In addition, unlike LiDAR, which provides a 3D point cloud, cameras can capture both 3D information and color information. This enables robots to recognize and differentiate objects based on color and texture. The 3D information capturing ability paves the way for cameras to replace LiDAR.

- High costs of LiDAR hardware encourage end-users to adopt alternative technologies. Cost is a major factor in the shift away from LiDAR. LiDAR sensors can be expensive, with prices ranging from a few hundred to several thousand dollars. In comparison, cameras are much more affordable, making them a more accessible option for many companies. This has resulted in the wider adoption of camera-based systems, as they are now more cost-effective for smaller companies and start-ups (which a lot of robot OEMs are). Nevertheless, despite the low costs of camera hardware (image sensors), the total cost of ownership can be extremely high for cameras because of the software and image processing units such as GPUs and image processing software systems.

- Size and weight. Cameras also have a smaller form factor compared to LiDAR, making them easier to integrate into mobile robots. This allows for more compact and lightweight designs, which can be crucial for robots that need to navigate through tight spaces or narrow doorways. Additionally, cameras can be placed in multiple locations on the robot, providing a wider field of view and improving navigation accuracy.

- Maintenance. Cameras are easier to calibrate and maintain compared to LiDAR. LiDAR requires careful alignment to ensure that the 3D point cloud is accurate, and it can be difficult to maintain that accuracy over time. On the other hand, cameras are typically plug-and-play, making them easier to use and maintain.

However, despite the superiorities mentioned above, IDTechEx's recent research, "Sensors for Robotics 2023-2043: Technologies, Markets, and Forecasts", also outlines a few barriers holding back the camera's adoption.

- High costs of software and other image processing units. Although image sensors cost considerably lower than LiDAR, the total cost of ownership of cameras, along with image processing units (software and GPUs), can lead to a high total cost of up to a few thousand dollars. In addition, in order to make cameras function in a robust manner, a solid machine vision system is needed. Unlike Tesla and John Deere, many robot OEMs have limited cash flow, making them conservative in investing too much capital on developing machine vision software. They would prefer to use existing LiDAR solutions.

- Data privacy. Many warehouse owners are hesitant to deploy mobile robots with cameras into their warehouses due to data privacy concerns. The lack of interest from end users slows down the adoption of cameras in robots. Furthermore, the lack of images and data collected from warehouses due to data privacy also makes it harder for robot OEMs to develop a robust machine vision system.

In conclusion, the shift towards camera-based systems for indoor mobile robots is a reflection of the changing priorities in the field. As costs come down and technology improves, cameras are becoming a more accessible and effective solution for indoor navigation and mapping. While LiDAR will likely still have a place in some applications and cameras present their own issues in the short term, it's clear that cameras are poised to become the dominant sensor for indoor mobile robots in the coming years. IDTechEx's report, "Sensors for Robotics 2023-2043: Technologies, Markets, and Forecasts", forecasts that the market size of cameras used in robots will have a 23-fold increase over the upcoming decade.

To find out more about this IDTechEx report, including downloadable sample pages, please visit www.IDTechEx.com/RoboticSensors.