This report has been updated. Click here to view latest edition.

If you have previously purchased the archived report below then please use the download links on the right to download the files.

電気トラック市場 2021-2041年

中型および大型のBEV、PHEVおよびFCEVの電気トラック市場の分析、詳細なコロナ禍対応修正後の売上額、バッテリー需要および地域別市場価値見通し、リチウムイオンおよび電動モーター技術

- By truck weight: with separate medium and heavy-duty forecasts

- By technology: battery electric, plug-in hybrid and fuel cell electric trucks.

- By geography: The US, China, Europe (EU + EFTA+UK) and the RoW as well as a aggregate global forecast.

- 20-year outlook: sales, market penetration (%), market revenue ($) and battery demand (GWh)

| 1. | EXECUTIVE SUMMARY |

| 1.1. | Electric Trucks: Drivers and Barriers |

| 1.2. | Road Freight Market |

| 1.3. | Global CO2 emission: medium & heavy duty trucks |

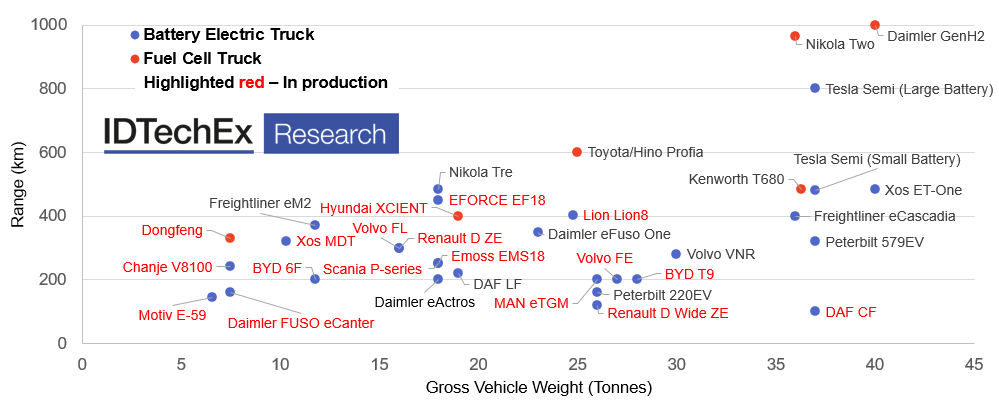

| 1.4. | Range of zero emission medium and heavy trucks |

| 1.5. | Heavy-duty: BEV or fuel cell? |

| 1.6. | Trucks and Covid-19 |

| 1.7. | Electric Trucks and Covid-19 |

| 1.8. | Key global forecast takeaways |

| 1.9. | Key regional forecast takeaways |

| 1.10. | MD & HD Truck Market Penetration 2017-2041 |

| 1.11. | MD & HD Truck Unit Sales 2017-2041 (BEV, PHEV, FCEV) |

| 1.12. | Electric MD & HD Truck Battery Demand 2017-2041 (GWh) |

| 1.13. | eM&HDT sales by region (000s units) |

| 1.14. | Electric MD & HD Truck Market Value 2017-2041 ($ Billion) |

| 1.15. | Commentary |

| 2. | INTRODUCTION |

| 2.1. | Electric Vehicle Terms |

| 2.2. | Electric Vehicles: Basic Principle |

| 2.3. | Electric Vehicles: Typical Specs |

| 2.4. | Types of popular on-road truck |

| 2.5. | A category that is difficult to define |

| 2.6. | Different segments of goods transportation by land |

| 2.7. | Truck classifications |

| 2.8. | Truck type |

| 2.9. | Truck axle layout descriptions |

| 2.10. | The Core Driver: Climate Change |

| 2.11. | Global CO2 emission: medium & heavy-duty trucks |

| 2.12. | CO2 emission from road transport, EU |

| 2.13. | GHG emission from the truck sector |

| 2.14. | Urban air quality |

| 2.15. | Fossil Fuel Bans (Cities) |

| 2.16. | Fossil Fuel Bans: Explained |

| 2.17. | Official or Legislated Fossil Fuel Bans (National) |

| 2.18. | Unofficial, Drafted or Proposed Fossil Fuel Bans (National) |

| 2.19. | The worldwide freight transport industry |

| 2.20. | Road Freight Market |

| 2.21. | Projected increase in global road freight activity |

| 2.22. | The rise of e-commerce: increased freight demand |

| 2.23. | Fuel / emissions regulation for new trucks |

| 2.24. | Fuel / CO2 emissions regulation for new trucks |

| 2.25. | December 2018: EU agrees 30% cut in truck CO2 emissions |

| 2.26. | Emissions regulation for new trucks - other pollutants |

| 2.27. | Fuel Saving Technology Areas |

| 2.28. | The rise of zero (or near zero) exhaust emission trucks |

| 2.29. | EU initiatives to offset additional powertrain weight |

| 3. | MEDIUM & HEAVY-DUTY TRUCKS IN EUROPE |

| 3.1. | Overview |

| 3.1.1. | Main truck brands in Europe |

| 3.1.2. | Medium and Heavy-Duty Truck Sales in the EU |

| 3.1.3. | The freight transport industry - Europe |

| 3.2. | Europe eTruck Players |

| 3.2.1. | Electric Trucks: MAN (VW GROUP) |

| 3.2.2. | Electric Trucks: SCANIA (VW GROUP) |

| 3.2.3. | Scania and Northvolt partnership |

| 3.2.4. | Electric Trucks: VOLVO |

| 3.2.5. | Electric Trucks: RENAULT TRUCKS (VOLVO) |

| 3.2.6. | Renault Trucks: Decades Before Electric Long Haul? |

| 3.2.7. | Biofuels and displacement fuels a stepping stone? |

| 3.2.8. | Renault BEV Refuge Truck at EVS 32 |

| 3.2.9. | Electric Trucks: MERCEDES (DAIMLER) |

| 3.2.10. | FUSO eCanter |

| 3.2.11. | Daimler eActros |

| 3.2.12. | Daimler eActros "innovation fleet" |

| 3.2.13. | Electric Trucks: IVECO |

| 3.2.14. | Electric Trucks: DAF (PACCAR) |

| 3.2.15. | Electric Trucks: E-FORCE ONE |

| 3.2.16. | Electric Trucks: FRAMO |

| 3.2.17. | Electric Trucks: TERBERG |

| 3.2.18. | Electric Trucks: ARRIVAL |

| 3.2.19. | Electric Trucks: EMOSS |

| 3.2.20. | Electric Trucks: TEVVA |

| 4. | MEDIUM & HEAVY-DUTY TRUCKS IN THE US |

| 4.1. | Overview |

| 4.1.1. | Main truck brands in the US |

| 4.1.2. | Main truck brands in the US in 2019 |

| 4.1.3. | Medium and Heavy-Duty Truck Sales in the US |

| 4.1.4. | The freight transport industry - US |

| 4.1.5. | Industry issues according to US truckers |

| 4.1.6. | Average truck replacement age in the US |

| 4.1.7. | Alternative fuel choices for trucks in the US |

| 4.1.8. | The cost of trucking in the United States |

| 4.1.9. | Average US On-Highway Diesel Prices 2000-Sep2020 |

| 4.1.10. | Running cost for US truckers |

| 4.1.11. | Nobody wants to be a truck driver in the US |

| 4.1.12. | The solution: electric, autonomous trucks? |

| 4.1.13. | California's Advanced Clean Trucks Regulation |

| 4.1.14. | CARB Voucher Incentive Project |

| 4.2. | US eTruck Players |

| 4.2.1. | Electric Trucks: FREIGHTLINER (DAIMLER) |

| 4.2.2. | Electric Trucks: PETERBILT (PACCAR) |

| 4.2.3. | Electric Trucks: VOLVO |

| 4.2.4. | Electric Trucks: MACK (VOLVO) |

| 4.2.5. | Electric Trucks: INTERNATIONAL (NAVISTAR) |

| 4.2.6. | Electric Trucks: TESLA |

| 4.2.7. | Electric Trucks: XOS TRUCKS |

| 4.2.8. | Electric Trucks: ALKANE |

| 4.2.9. | Electric Trucks: LION ELECTRIC |

| 4.2.10. | Electric Trucks: CUMMINS |

| 4.2.11. | Electric Trucks: WRIGHTSPEED |

| 4.2.12. | Electric Trucks: ZEROTRUCK |

| 4.2.13. | Electric Trucks: CHANJE |

| 4.2.14. | Electric Trucks: EDI |

| 4.2.15. | Motiv Power Systems - Medium Duty eTrucks |

| 4.2.16. | Electric Trucks: ORANGE EV |

| 4.2.17. | TransPower - Heavy Duty Class 8 eTrucks |

| 4.2.18. | Electric Trucks: TransPower |

| 4.2.19. | Electric Trucks: LIGHTNING SYSTEMS |

| 4.2.20. | Rivian / Amazon electric delivery van |

| 5. | MEDIUM & HEAVY-DUTY TRUCKS IN CHINA |

| 5.1. | Overview |

| 5.1.1. | Main truck brands in China |

| 5.1.2. | Medium and Heavy-Duty Truck Sales in China |

| 5.1.3. | The worldwide freight transport industry - China |

| 5.1.4. | The freight transport industry - China |

| 5.1.5. | Truck engine supplier relationships in China |

| 5.1.6. | Chinese truck joint ventures |

| 5.1.7. | China's truck market segments |

| 5.1.8. | Total Commercial Vehicle Sales in China |

| 5.2. | China eTruck Players |

| 5.2.1. | Electric Trucks: FAW JIEFANG |

| 5.2.2. | Electric Trucks: DONGFENG |

| 5.2.3. | Electric Trucks: SINOTRUCK CDW |

| 5.2.4. | Electric Trucks: SHACMAN |

| 5.2.5. | Electric Trucks: FOTON |

| 5.2.6. | Electric Trucks: JAC MOTORS |

| 5.2.7. | Electric Trucks: DAYUN |

| 5.2.8. | Electric Trucks: GEELY |

| 5.2.9. | Electric Trucks: BYD |

| 5.2.10. | Electric Trucks: CHTC Chufeng |

| 6. | MEDIUM & HEAVY-DUTY TRUCKS: ROW |

| 6.1.1. | Main truck brands in Japan |

| 6.1.2. | Japan truck market share by manufacturer |

| 6.1.3. | Historic truck sales in Japan |

| 6.1.4. | Truck transport business in Japan |

| 6.1.5. | Russian Truck Fleet |

| 6.1.6. | Historic truck sales in Russia |

| 6.1.7. | Russia truck market share by manufacturer |

| 6.1.8. | Historic truck sales in India |

| 6.1.9. | India truck market share by manufacturer |

| 6.1.10. | Mexico |

| 6.1.11. | Electric Trucks: HINO MOTORS |

| 6.1.12. | Electric Trucks: HYUNDAI |

| 7. | TCO CONSIDERATIONS |

| 7.1. | Advantages and disadvantages of electric vs. fuel cell trucks |

| 7.2. | TCO considerations for electric trucks |

| 7.3. | Cost projections in selected countries for various powertrains |

| 7.4. | Electric trucks reduced operating costs |

| 7.5. | TCO of a diesel vs. an all-electric Class 6 truck |

| 7.6. | TCO of a diesel vs. an all-electric tractor-trailer |

| 7.7. | Overcoming barriers for low emission technologies |

| 7.8. | More carrot, more stick |

| 8. | LI-ION BATTERIES |

| 8.1. | Overview |

| 8.1.1. | What is a Li-ion battery? |

| 8.1.2. | The Battery Trilemma |

| 8.1.3. | Electrochemistry Definitions |

| 8.1.4. | Lithium-based Battery Family Tree |

| 8.1.5. | Battery Wish List |

| 8.1.6. | More Than One Type of Li-ion battery |

| 8.1.7. | NMC: from 111 to 811 |

| 8.1.8. | Cobalt: Price Volatility |

| 8.1.9. | Cathode Performance Comparison |

| 8.1.10. | 811 Commercialisation Examples |

| 8.1.11. | Commercial Anodes: Graphite |

| 8.1.12. | The Promise of Silicon-based Anodes |

| 8.1.13. | The Reality of Silicon |

| 8.1.14. | Silicon: Incremental Steps |

| 8.1.15. | What is in a Cell? |

| 8.1.16. | Inactive Materials Negatively Affect Energy Density |

| 8.1.17. | Commercial Battery Packaging Technologies |

| 8.1.18. | Comparison of Commercial Cell Geometries |

| 8.1.19. | What is NCMA? |

| 8.1.20. | Lithium-based Batteries Beyond Li-ion |

| 8.1.21. | Li-ion Chemistry Snapshot: 2020, 2025, 2030 |

| 8.2. | Commercial Battery Pack Players |

| 8.2.1. | LithiumWerks: Standing Outside the Party |

| 8.2.2. | LithiumWerks' Battery Cells |

| 8.2.3. | LithiumWerks' Battery Cells: Made in China |

| 8.2.4. | Akasol Emerging as Key Supplier for Commercial EVs |

| 8.2.5. | Akasol Energy Density Road Map for Commercial EVs |

| 8.2.6. | Akasol's 'Answer to Solid State' |

| 8.2.7. | Leclanché: Premium Battery Maker |

| 8.2.8. | Forsee Power: Struggling to Stand Out |

| 8.2.9. | Webasto Expanding Production |

| 8.2.10. | EnerDel: battery packs for trucks |

| 9. | BATTERY CHOICE FOR ELECTRIC TRUCKS |

| 9.1. | LFP or High-Nickel Cathodes for eTrucks? |

| 9.2. | Electric Truck OEM Battery Chemistry Choice |

| 9.3. | Heavy-Duty Battery Choice: Range & Payload |

| 9.4. | Heavy-Duty Battery Choice: Charging |

| 9.5. | Heavy-Duty Battery Choice: Cost |

| 9.6. | Heavy-Duty Battery Choice: Reliability |

| 9.7. | Supply Chain Examples: In-House Pack Assembly |

| 9.8. | Supply Chain Examples: In-House Pack & Cell Assembly |

| 9.9. | Supply Chain Examples: External Pack Assembly |

| 9.10. | Chemistry choice - Europe and North America |

| 9.11. | Battery Chemistry Tailored to Duty Requirement |

| 9.12. | Timeline and Outlook For Li-ion Energy Densities |

| 9.13. | China Electric Heavy-Duty Truck Battery Suppliers |

| 9.14. | CATL & BYD Dominate eBus Battery Market |

| 9.15. | Chinese Battery Manufacturers for eBuses |

| 10. | CHARGING |

| 10.1. | Charging methods |

| 10.2. | MW Charging Difficulty for BEVs |

| 10.3. | The emergence of 'Mega chargers' |

| 10.4. | Siemens eHighway |

| 10.5. | There's Now An Electric Highway In California |

| 10.6. | Mack demonstrates catenary-powered PHEV |

| 10.7. | Volvo's electric roads point to battery-free EV future |

| 10.8. | Qualcomm - dynamic charging |

| 10.9. | Daimler Truck opened charging park for commercial EVs |

| 10.10. | CharIN is working on charging standard for commercial electric vehicles |

| 10.11. | Momentum Dynamics: high-power wireless charging for electric vehicle fleets |

| 10.12. | Types of electric road systems |

| 10.13. | Electric road systems: conductive versus inductive |

| 10.14. | Electric road systems: Sweden |

| 10.15. | Germany tests its first electric highway for trucks |

| 10.16. | Electric road systems: market and challenges |

| 11. | ELECTRIC TRACTION MOTORS |

| 11.1. | Comparison of Traction Motor Construction and Merits |

| 11.2. | Motor Efficiency Comparison |

| 11.3. | Magnet Price Increase? |

| 11.4. | LCVs & Trucks |

| 11.5. | Motors per Vehicle and kWp per Vehicle Assumptions |

| 11.6. | Brushed DC: Small Presence in LCVs |

| 11.7. | LCVs and Trucks Motor Outlook |

| 12. | FUEL CELLS |

| 12.1. | Proton Exchange Membrane Fuel Cells |

| 12.2. | Fuel Cell Inefficiency and Cooling Methods |

| 12.3. | Challenges for Fuel Cells |

| 12.4. | Grey Hydrogen |

| 12.5. | Case Study: Hydrogen Costs |

| 12.6. | Infrastructure Costs |

| 12.7. | Fuel Cell Charging Infrastructure in the US |

| 12.8. | Fuel Cost per Mile: FCEV, BEV, internal-combustion |

| 12.9. | Fuel cells and trucks today |

| 12.10. | Primary issues for battery and fuel cell trucks |

| 12.11. | Batteries vs. Fuel Cells: driving range |

| 12.12. | Guide to hydrogen truck refuelling |

| 12.13. | Developing hydrogen refuelling infrastructure |

| 12.14. | Nikola Trucks: Hydrogen Infrastructure |

| 12.15. | Alternative fuels generation - 2030 vs. 2050 |

| 12.16. | Using bio-waste to generate hydrogen |

| 12.17. | Timeline for Nikola |

| 12.18. | First Nikola truck will be a BEV (not fuel cell) |

| 12.19. | Nikola One |

| 12.20. | Nikola Commercial Truck Milestones |

| 12.21. | Nikola TWO: New Flagship Fuel Cell Truck |

| 12.22. | Nikola BEV Garbage Truck Order |

| 12.23. | Nikola an "Energy Technology Company"? |

| 12.24. | IDTechEx Take: The Future for Nikola |

| 12.25. | Fuel Cell Trucks: KENWORTH (PACCAR) |

| 12.26. | Fuel Cell Trucks: BALLARD / UPS |

| 12.27. | Fuel Cell Trucks: DONGFENG |

| 12.28. | Fuel Cell Trucks: HYUNDAI |

| 12.29. | Fuel Cell Trucks: DAIMLER / VOLVO |

| 12.30. | Fuel Cell Trucks: TOYOTA / HINO |

| 12.31. | Arcola Energy |

| 12.32. | ULEMCo Ltd |

| 12.33. | Fuel Cell Truck Example Specifications |

| 13. | 2020 ETRUCK SALES UPDATE |

| 13.1. | European Electric Truck Sales 2016-2020 |

| 13.2. | Addressable Truck Market: Europe Market Share 2020 |

| 13.3. | Medium and Heavy-Duty Truck Sales in Europe |

| 13.4. | TRATON GROUP Electric Truck Orders H1 2021 |

| 13.5. | VOLVO Group H1 2021 |

| 13.6. | Main Truck Brands in the U.S. |

| 13.7. | Addressable Truck Market: U.S. Market Share 2020 |

| 13.8. | Medium and Heavy-Duty Truck Sales in the U.S. |

| 13.9. | U.S. Electric Truck Sales 2016-2020 |

| 13.10. | U.S. Electric Trucks Manufacturers |

| 13.11. | China Heavy-Duty Electric Truck Sales in 2020 |

| 13.12. | Electric Heavy-Duty Truck Sales in China 2020 |

| 13.13. | Electric Heavy-Duty Truck Sales in China 2021 |

| 13.14. | Addressable Truck Market: China HDT Market Share 2020 |

| 13.15. | Medium and Heavy-Duty Truck Sales in China |

| 13.16. | Recovery from Coronavirus: Addressable Truck Market |

| 13.17. | Truck OEMs Commit to Electrification |

| 13.18. | Volvo Trucks |

| 13.19. | Daimler Trucks & Buses |

| 13.20. | Traton Group |

| 13.21. | PACCAR |

| 13.22. | CNH Industrial / IVECO / Nikola |

| 13.23. | TESLA |

| 13.24. | BYD |

| 14. | FORECASTS |

| 14.1. | Overview |

| 14.1.1. | Forecast Assumptions |

| 14.1.2. | Forecast Methodology |

| 14.1.3. | Battery Shortage Assumptions |

| 14.1.4. | Li-ion Cell and Pack Price Assumptions 2020-2030 |

| 14.1.5. | Market forecast: Average battery capacity for electric medium-duty trucks (kWh) 2020-2041 |

| 14.1.6. | Market forecast: Average battery capacity for electric heavy-duty trucks (kWh) 2020-2041 |

| 14.1.7. | Market forecast: Average battery capacity for medium- and heavy-duty fuel cell electric trucks (kWh) 2020-2041 |

| 14.1.8. | Market forecast: Average battery capacity for medium- and heavy-duty PHEV trucks (kWh) 2020-2041 |

| 14.2. | Medium and Heavy-Duty Truck Market Forecasts 2021-2041 |

| 14.2.1. | M&HDT global sales (000s units) |

| 14.2.2. | M&HDT global sales: BEV, PHEV and FCEV (000s) |

| 14.2.3. | eM&HDT sales by region (000s units) |

| 14.2.4. | M&HDT market share forecast for eM&HDT (%) |

| 14.2.5. | eM&HDT battery demand forecast (GWh) |

| 14.2.6. | eM&HDT battery demand forecast by region (GWh) |

| 14.2.7. | eM&HDT market forecast ($US billion) |

| 14.2.8. | eM&HDT market forecast by region ($US billion) |

| 14.2.9. | FCEV M&HDT Fuel Cell Demand Forecast (MW) |

| 14.3. | Medium-Duty Truck Market Forecasts 2021-2041 |

| 14.3.1. | MDT global sales (000s units) |

| 14.3.2. | eMDT sales: BEV, PHEV and FCEV (000s) |

| 14.3.3. | eMDT sales by region (000s units) |

| 14.3.4. | MDT market share forecast for eMDT |

| 14.3.5. | eMDT battery demand forecast (GWh) |

| 14.3.6. | eMDT battery demand forecast by region (GWh) |

| 14.3.7. | eMDT market forecast ($US billion) |

| 14.3.8. | eMDT market forecast by region ($US billion) |

| 14.3.9. | FCEV MDT Fuel Cell Demand Forecast (MW) |

| 14.4. | Heavy-Duty Truck Market Forecasts 2021 2041 |

| 14.4.1. | HDT global sales (000s units) |

| 14.4.2. | eHDT sales: BEV, PHEV and FCEV (000s) |

| 14.4.3. | eHDT sales by region (000s units) |

| 14.4.4. | HDT market share forecast for eHDT |

| 14.4.5. | eHDT battery demand forecast (GWh) |

| 14.4.6. | eHDT battery demand forecast by region (GWh) |

| 14.4.7. | eHDT market forecast ($US billion) |

| 14.4.8. | eHDT market forecast by region ($US billion) |

| 14.4.9. | FCEV HDT Fuel Cell Demand Forecast (MW) |

| 14.5. | Regional Sales Forecasts 2021-2041 |

| 14.5.1. | Europe MDT sales (000s units) |

| 14.5.2. | Europe HDT sales (000s units) |

| 14.5.3. | US MDT sales (000s units) |

| 14.5.4. | US HDT sales (000s units) |

| 14.5.5. | China MDT sales (000s units) |

| 14.5.6. | China HDT sales (000s units) |

| 14.5.7. | RoW MDT sales (000s units) |

| 14.5.8. | RoW HDT sales (000s units) |

レポート概要

| スライド | 363 |

|---|---|

| フォーキャスト | 2041 |

お客様の声