This report has been updated. Click here to view latest edition.

If you have previously purchased the archived report below then please use the download links on the right to download the files.

電気自動車用パワーエレクトロニクス 2023年-2033年

自動車電力用半導体素子、Si、SiC、GaN、電源モジュール、ディスクリート、電気自動車、インバータ、OBC。

- 現在・未来のパッケージ材料(OEMケーススタディ含む)

- 主要企業の一次情報

- インバータ、車載充電器(OBC)、DC/DCコンバータの売上台数、GWと米ドル換算。電圧別(600V、1200V)と半導体タイプ別(Si、SiC、GaN)の需要規模

- 電力レベル別OBC見通し: 4kW、6-11.5kW、16-22kW

- インバータ、OBC、コンバータ、Si、SiC、GaN、コスト見通し(kW毎ドル)

- 平均的インバータ/車両

- インバータ用ディスクリートモジュールと電源モジュール 2020-2033年

- AC/DC充電設備設置(グローバル)

- インバータ冷却方法: 空冷、油冷、水グリコール系液冷

- Electric vehicle markets: regional trends & future growth

- Supply chain for power semiconductor materials, devices & OEMs

- Evolution of package materials & thermal management: die-attach, wire bonding, TIM, water/oil cooling and more

- High voltage platform (800V) market drivers & future developments

- Company profiles including interviews

- Forecasts 2023-2033: Unit sales, GW and US$ demand for inverters, onboard chargers (OBC) and DC-DC converters segmented by voltage (600V, 1200V) and semiconductor type (Si, SiC, GaN).

- Forecasts 2023-2033: OBC by Power Level: 4kW, 6-11.5kW, 16-22kW

- Forecasts 2023-2033: Inverter, OBC & Converter, Si, SiC, GaN, Cost Outlook (US$ per kW)

- Forecasts 2023-2033: AC & DC Charging infrastructure installations (Global)

- Forecasts 2023-2033: Inverter cooling strategy: air, oil, water-glycol

| 1. | EXECUTIVE SUMMARY |

| 1.1. | Report Introduction |

| 1.2. | Power Electronics in Electric Vehicles |

| 1.3. | Benchmarking Silicon, Silicon Carbide & Gallium Nitride Semiconductors |

| 1.4. | Power Electronics & Battery Shortages |

| 1.5. | SiC Drives 800V Platforms |

| 1.6. | EV Markets Surge in 2022 |

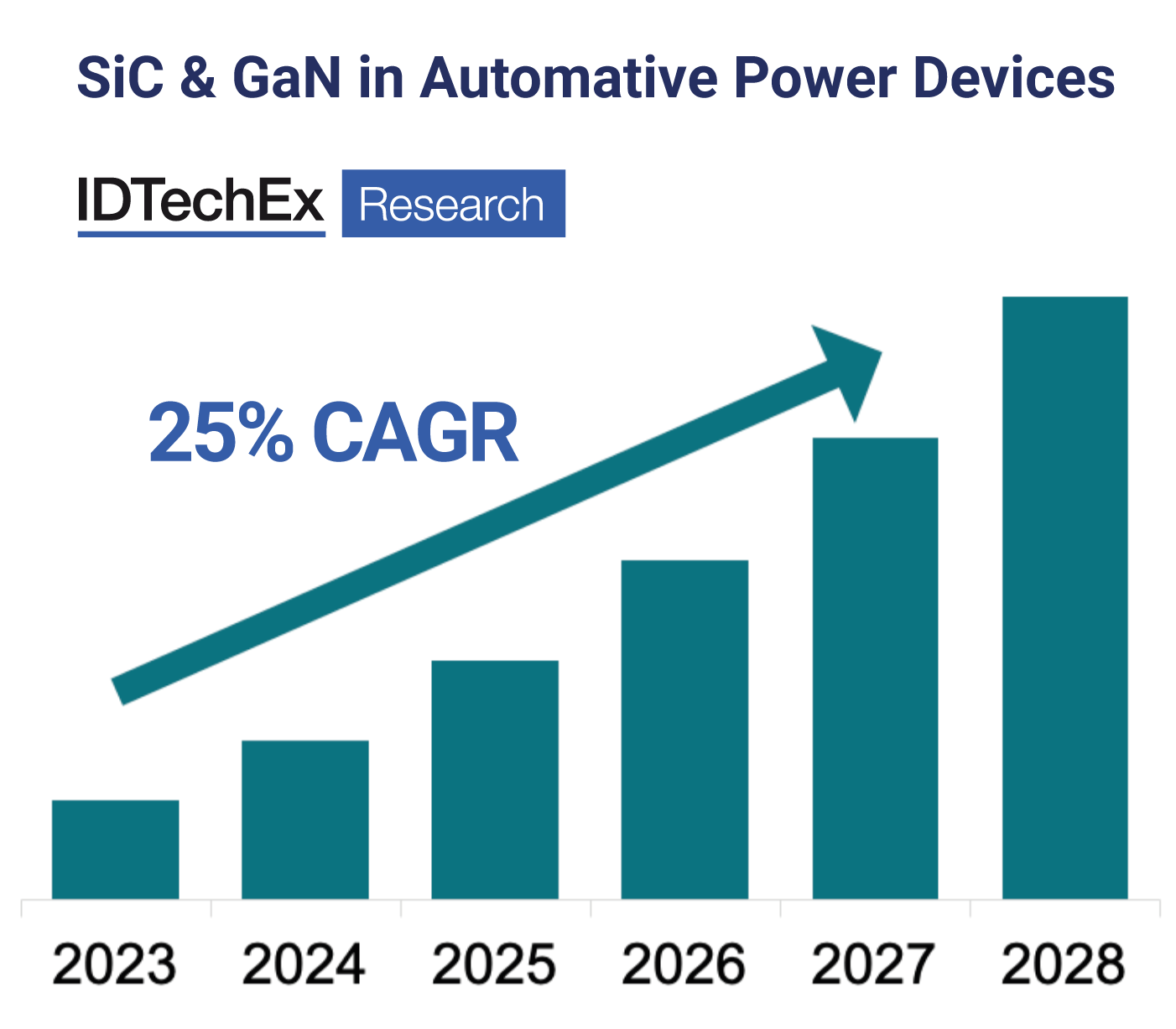

| 1.7. | Inverter Forecast 2020-2033 (GW): GaN 600V, Si IGBT 600V, SiC MOSFET 600V, 1200V |

| 1.8. | Discretes vs Power Modules for Inverters 2020-2033 |

| 1.9. | Inverter Power Density Increases Over Time |

| 1.10. | Automotive: Key Application for Sintering |

| 1.11. | Power Electronics: Materials Trends Overview |

| 1.12. | Inverter Market Share 2020-2033: GaN 600V, Si IGBT 600V, SiC MOSFET 600V, 1200V |

| 1.13. | 800V Model Announcements in China (2022) |

| 1.14. | Evolving SiC Supply Relationships |

| 1.15. | OBC by Level: 4kW, 6-11.5kW, 16-22kW 2023- 2033 |

| 1.16. | OBC & DC-DC Converter: Si, SiC, GaN 2020 - 2033 (GW) |

| 1.17. | Inverter, OBC, DC-DC Converter 2020-2023 (GW) |

| 1.18. | Inverter, OBC, DC-DC Converter 2020-2023 (US$ billion) |

| 1.19. | IDTechEx Company Profiles |

| 2. | ELECTRIC VEHICLE MARKETS: REGIONAL TRENDS & FUTURE GROWTH |

| 2.1. | Electric Vehicle Definitions |

| 2.2. | Electric Vehicles: Typical Specs |

| 2.3. | Exponential Growth in Regional EV Markets |

| 2.4. | Summary of Regional Trends & Drivers for EVs in 2022 |

| 2.5. | Regional Trends: China |

| 2.6. | NEV Sales by Vehicle Class |

| 2.7. | The Dual-Credit System (1) |

| 2.8. | The Dual-Credit System (2) |

| 2.9. | Regional Trends: EU + UK + EFTA |

| 2.10. | Europe Emissions Standards |

| 2.11. | EU ICE Ban by 2035 |

| 2.12. | EU 'Fit for 55' |

| 2.13. | Regional Trends: US |

| 2.14. | Electric Pickups - The Next Big Thing |

| 2.15. | Hybrid Car Sales Surges |

| 2.16. | Powertrain Tailpipe Emissions Comparison |

| 2.17. | Automaker & Government EV Targets |

| 2.18. | Cars: Total Cost of Ownership |

| 2.19. | Shortages Across the Supply Chain |

| 2.20. | Grid Emissions (1) |

| 2.21. | Grid Emissions (2) |

| 2.22. | Chip Shortages - Background |

| 2.23. | Semiconductor Content Increased |

| 3. | OVERVIEW OF EV POWER ELECTRONICS & WBG SEMICONDUCTORS |

| 3.1. | What is Power Electronics? |

| 3.1.1. | Power Electronics Use in Electric Vehicles |

| 3.1.2. | Transistor History & MOSFET Overview |

| 3.1.3. | Wide Bandgap (WBG) Semiconductor Advantages & Disadvantages |

| 3.1.4. | Benchmarking Silicon, Silicon Carbide & Gallium Nitride Semiconductors |

| 3.1.5. | Advantages of SiC Material |

| 3.1.6. | Limitations of SiC Power Devices |

| 3.1.7. | GaN's Potential to Reach High Voltage |

| 3.1.8. | SiC & GaN Have Substantial Room for Improvement |

| 3.1.9. | Automotive GaN Device Suppliers are Growing |

| 3.1.10. | GaN to Become Preferred OBC Technology |

| 3.1.11. | Challenges for GaN Devices |

| 3.1.12. | SiC Power Roadmap |

| 3.1.13. | Applications Summary for WBG Devices |

| 3.2. | Inverter, OBC, Converter Design & Si, SiC, GaN Outlook |

| 3.2.1. | Inverter Overview |

| 3.2.2. | Pulse Width Modulation |

| 3.2.3. | Traditional EV Inverter |

| 3.2.4. | Discretes & Modules |

| 3.2.5. | Inverter Printed Circuit Boards |

| 3.2.6. | Electric Vehicle Inverter Benchmarking |

| 3.2.7. | SiC Impact on the Inverter Package |

| 3.2.8. | Inverter Forecast 2020 - 2033 (GW): GaN 600V, Si IGBT 600V, SiC MOSFET 600V, 1200V |

| 3.2.9. | OBC & DC-DC Converter: Si, SiC, GaN 2020-2033 (GW) |

| 3.2.10. | Onboard Charger Circuit Components |

| 3.2.11. | Tesla Onboard Charger / DC-DC Converter |

| 3.2.12. | OBC by Level: 4kW, 6-11.5kW, 16-22kW 2023- 2033 |

| 4. | SUPPLY CHAIN FOR POWER SEMICONDUCTOR MATERIALS, DEVICES & OEMS |

| 4.1. | Automotive Power SC Supplier Market Shares |

| 4.2. | Evolving SiC Supply Relationships |

| 4.3. | SiC Supply Chain in 2023 |

| 4.4. | Infineon CoolSiC Efficiency Gains |

| 4.5. | Infineon Establishing Major OEM Partnerships |

| 4.6. | Hyundai Diversifies SiC Supply for Best-Selling 800V E-GMP Platform |

| 4.7. | ROHM Semiconductor Expands SiC Production Capacity |

| 4.8. | STMicroelectronics Releases ACEPACK in Race for Market Leadership |

| 4.9. | Wolfspeed: Major Investment & OEM Partnerships for SiC |

| 4.10. | Delphi Technologies (BorgWarner) Supply Luxury Automakers with Viper SiC Module |

| 4.11. | BorgWarner Integrated Drive Module for Ford |

| 4.12. | On Semi EliteSiC |

| 4.13. | GM From Bolt & Volt to Ultium |

| 4.14. | Hitachi Double Sided IGBTs to Major OEM |

| 4.15. | Volvo Heavy Duty SiC Inverter |

| 4.16. | Continental / Jaguar Land Rover |

| 4.17. | Nissan Leaf Custom Design |

| 5. | POWER ELECTRONICS PACKAGES: EV USE-CASES |

| 5.1. | Toyota Prius 2004-2010 |

| 5.2. | 800V Si IGBT Choices |

| 5.3. | 2008 Lexus |

| 5.4. | Toyota Prius 2010-2015 |

| 5.5. | Nissan Leaf 2012 |

| 5.6. | Honda Accord 2014 |

| 5.7. | Honda Fit (by Mitsubishi) |

| 5.8. | Toyota Prius 2016 Onwards |

| 5.9. | Chevrolet Volt 2016 (by Delphi) |

| 5.10. | Cadillac 2016 (by Hitachi) |

| 5.11. | BWM i3 (by Infineon) |

| 5.12. | STMicro |

| 5.13. | Continental / Jaguar Land Rover Inverter |

| 5.14. | Nissan Leaf Custom Inverter Design |

| 5.15. | Danfoss |

| 5.16. | BorgWarner |

| 5.17. | onsemi |

| 6. | EVOLUTION OF PACKAGE MATERIALS & THERMAL MANAGEMENT: DIE-ATTACH, WIRE BONDING, TIM, WATER/OIL COOLING AND MORE |

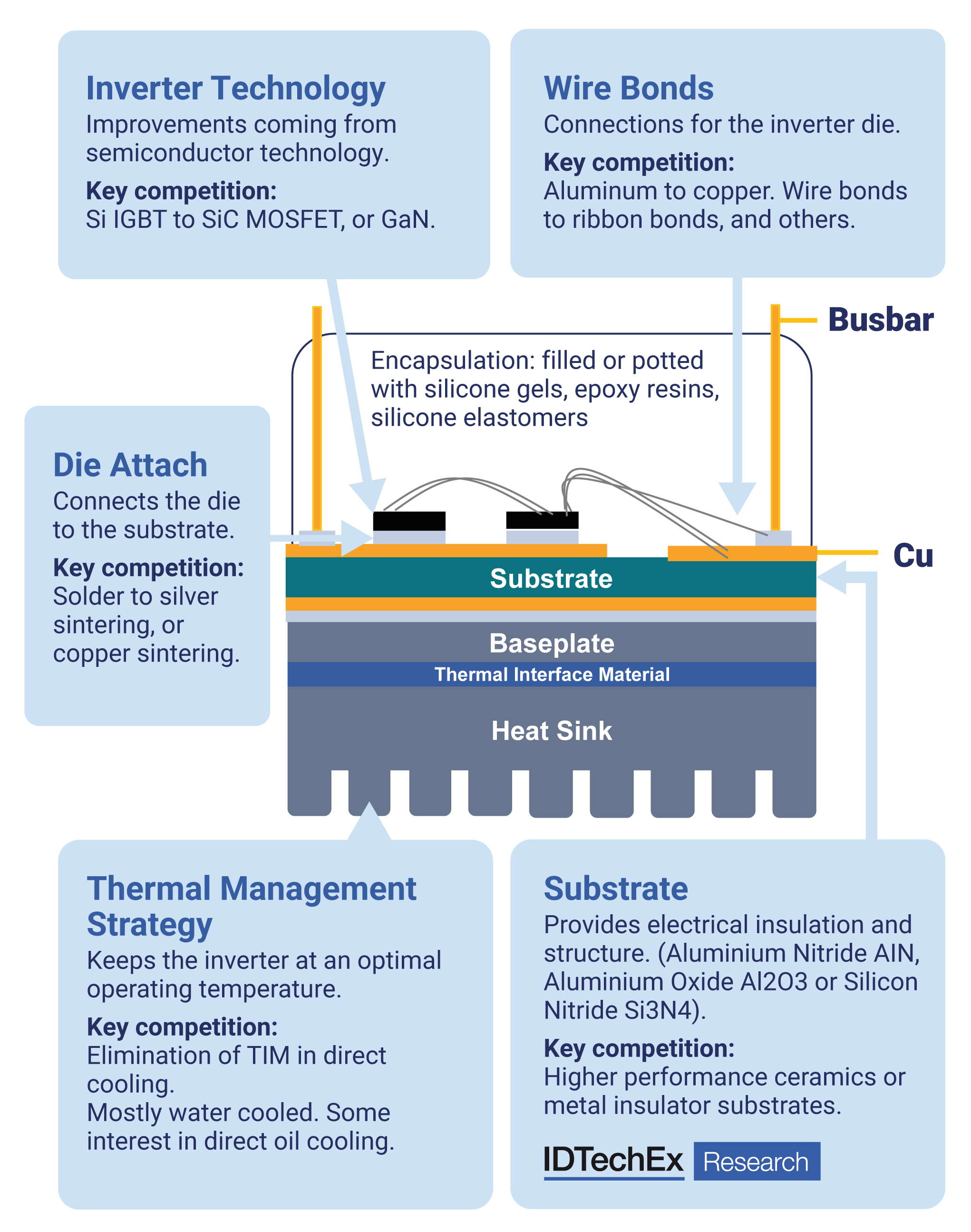

| 6.1. | Overview |

| 6.1.1. | Power Module Packaging Over the Generations |

| 6.1.2. | Power Electronics Material Evolution |

| 6.1.3. | Automotive: Key Application for Sintering |

| 6.1.4. | Module Packaging Material Dimensions |

| 6.1.5. | OEM Power Module Material Innovations |

| 6.1.6. | Die Attach Materials: Solder, Ag & Cu Sintering & Key Players |

| 6.1.7. | WBG Moves Beyond the Limits of SAC |

| 6.1.8. | Inverter Power Density Increases Over Time |

| 6.1.9. | Die and Substrate Attach are Common Failure Modes |

| 6.1.10. | Ag Sintering with WBG Semiconductors |

| 6.1.11. | Resolving Challenges with Ag Sintering |

| 6.1.12. | Nano Particle Ag Sinter |

| 6.1.13. | Power Module Supply Chain & Innovations |

| 6.1.14. | Summary of Ag sintering, Solder and TLPB |

| 6.1.15. | Toyo Chem: Sintered Die Attach Paste |

| 6.1.16. | LG: Ag Sintering Paste with Low Sintering Temperature |

| 6.1.17. | Amo Green: Pressure-less Nano Ag Sintering Paste |

| 6.1.18. | Indium Corp: Nano Ag Pressure-less Sinter Paste |

| 6.1.19. | Nihon Superior: Nano Silver for Sintering |

| 6.1.20. | Cu Sintering Pastes Improve Ag Sintered Performance |

| 6.1.21. | Hitachi: Cu Sintering Paste |

| 6.1.22. | Cu Sintering: Characteristics |

| 6.1.23. | Reliability of Cu Sintered Joints |

| 6.1.24. | Mitsui Mining: Nano Copper Pressured and Pressure-less Sintering Under N2 Environment |

| 6.1.25. | Mitsui Mining: Nano Copper Pressure-less Sintering Under N2 Environment |

| 6.1.26. | Die Attach Technology Trends |

| 6.1.27. | Wire Bond Evolution & Future Alternatives |

| 6.1.28. | Wire Bonds a Failure Point |

| 6.1.29. | Alternative Wire Bonding Techniques |

| 6.1.30. | Die Top System - Heraeus |

| 6.1.31. | Direct Lead Bonding (Mitsubishi) |

| 6.1.32. | Tesla Inverter Design Evolution |

| 6.1.33. | Embedded Lead Frames for Thermal Performance |

| 6.1.34. | Technology Evolution Beyond Al Wire Bonding |

| 6.2. | Substrate Materials & Future Alternatives |

| 6.2.1. | The Choice of Ceramic Substrate Technology |

| 6.2.2. | AlN: Overcoming its Mechanical Weakness |

| 6.2.3. | Thermal Conductivity vs Thermal Expansion |

| 6.2.4. | Ceramics: CTE Mismatch |

| 6.2.5. | Approaches to Metallisation: DPC, DBC, AMB and Thick Film Metallisation |

| 6.2.6. | Direct Plated Copper (DPC): Pros and Cons |

| 6.2.7. | Double Bonded Copper (DBC): Pros and Cons |

| 6.2.8. | Active Metal Brazing (AMB): Pros and Cons |

| 6.2.9. | Thick Film Printing |

| 6.2.10. | Heraeus - Materials for Power Electronics |

| 6.2.11. | ALMT - MgSiC Baseplate |

| 6.3. | Thermal Management |

| 6.3.1. | Optimal Temperatures for Multiple Components |

| 6.3.2. | Single Side, Double Side, Direct, and Direct Cooling |

| 6.3.3. | Double-Sided Cooling Examples |

| 6.3.4. | Baseplate, Heat sink, and Encapsulation Materials |

| 6.3.5. | Removing Thermal Interface Materials |

| 6.3.6. | Why TIM is Used in Power Electronics |

| 6.3.7. | Why the Drive to Eliminate the TIM? |

| 6.3.8. | Thermal Grease: Other Shortcomings |

| 6.3.9. | EV Inverter Modules Where TIM has Been Eliminated (1) |

| 6.3.10. | EV Inverter Modules Where TIM has Been Eliminated (2) |

| 6.3.11. | Infineon - Pre-Applied TIM |

| 6.3.12. | IGBTs and SiC are not the Only TIM Area in Inverters |

| 6.3.13. | Cooling power electronics: water or oil |

| 6.3.14. | Inverter Package Cooling |

| 6.3.15. | Drivers for Direct Oil Cooling of Inverters |

| 6.3.16. | Advantages, Disadvantages and Drivers for Oil Cooled Inverters |

| 6.3.17. | Direct Oil Cooling Projects |

| 6.3.18. | Inverter Cooling Strategy Forecast (Units) |

| 6.3.19. | Ford Mustang Mach-E |

| 6.3.20. | Fraunhofer and Marelli - Directly Cooled Inverter |

| 6.3.21. | Hitachi - Oil Cooled Inverter |

| 6.3.22. | Jaguar I-PACE 2019 |

| 6.3.23. | Lucid - Water Cooled Onboard Charger |

| 6.3.24. | Nissan Leaf |

| 6.3.25. | Renault Zoe 2013 (Continental) |

| 6.3.26. | Rivian |

| 6.3.27. | Senior Flexonics - IGBT Heat Sink Design |

| 6.3.28. | Tesla Model 3 |

| 6.3.29. | VW ID |

| 7. | HIGH VOLTAGE PLATFORM (800V) MARKET DRIVERS & FUTURE DEVELOPMENTS |

| 7.1. | SiC Drives 800V Platforms |

| 7.2. | Emerging 800V Platforms & SiC Inverters |

| 7.3. | Inverter Market Share 2020 - 2033: SiC 1200V, SiC 600V, GaN 600V, Si IGBT 600V |

| 7.4. | 800V Model Announcements in China (2022) |

| 7.5. | 800V For & Against |

| 7.6. | DCFC Impact on Li-ion Cells |

| 7.7. | Fast Charge Cell Design Hierarchy - Levers to Pull |

| 7.8. | DC Fast Charging Levels |

| 7.9. | AC & DC Charging Installations 2015-2032 |

| 7.10. | 800V Platform Discussion & Outlook |

| 8. | FORECASTS |

| 8.1. | Exponential Growth in Regional EV Markets |

| 8.2. | Methodology |

| 8.3. | Inverters per Car Forecast |

| 8.4. | Multiple Motors / Inverters per Vehicle |

| 8.5. | Inverter Forecast 2020 - 2033 (GW): GaN 600V, Si IGBT 600V, SiC MOSFET 600V, 1200V |

| 8.6. | Inverter Market Share 2020 - 2033: GaN 600V, Si IGBT 600V, SiC MOSFET 600V, 1200V |

| 8.7. | Inverter Cooling Strategy Forecast (Units) |

| 8.8. | Discretes vs Power Modules for Inverters 2020 - 2033 |

| 8.9. | OBC & DC-DC Converter: Si, SiC, GaN 2020 - 2033 (GW) |

| 8.10. | Inverter, OBC, DCDC Converter 2020 - 2023 (GW) |

| 8.11. | Inverter, OBC, DCDC Converter 2020 - 2023 (US$ billion) |

| 8.12. | OBC by Level: 4kW, 6-11.5kW, 16-22kW 2023- 2033 |

| 8.13. | Inverter, OBC & Converter, Si, SiC, GaN Cost Assumptions (US$ per kW) |

| 8.14. | AC & DC Charging Installations 2015-2032 |

| 9. | COMPANY PROFILES |

| 9.1. | Dynex |

| 9.2. | Efficient Power Conversion: GaN FETs |

| 9.3. | Elaphe |

| 9.4. | Equipmake |

| 9.5. | ESI Automotive |

| 9.6. | General Electric: Megawatt Converters |

| 9.7. | Infineon |

| 9.8. | IQE |

| 9.9. | Nexperia: GaN for EV Power Electronics |

| 9.10. | Power Electronics: EV Charging |

レポート概要

| スライド | 221 |

|---|---|

| フォーキャスト | 2033 |

お客様の声